อิทธิพลของการกำกับดูแลกิจการที่ดี คุณภาพการเปิดเผยข้อมูล นโยบายการจ่ายเงินปันผล และการจัดการกำไรที่ส่งผลต่อความไม่สมมาตรของข้อมูลในช่วงวิกฤต Covid-19

คำสำคัญ:

ความไม่สมมาตรของข้อมูล, การกำกับดูแลกิจการที่ดี, คุณภาพการเปิดเผยข้อมูล, นโยบายการจ่ายเงินปันผล, การจัดการกำไรบทคัดย่อ

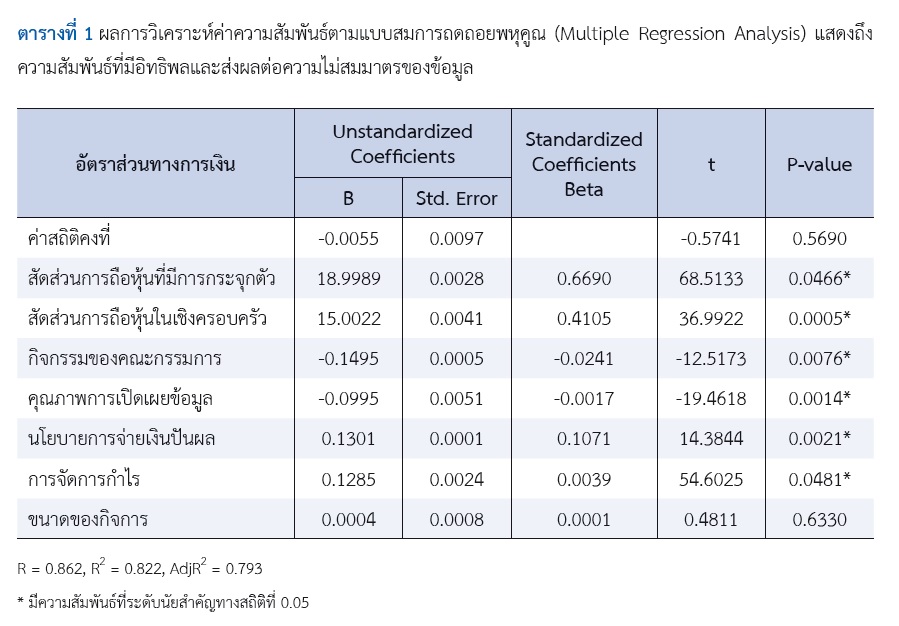

การศึกษาอิทธิพลของการกำกับดูแลกิจการที่ดี คุณภาพการเปิดเผยข้อมูล นโยบายการจ่ายเงิน ปันผลและการจัดการกำไรที่ส่งผลต่อความไม่สมมาตรของข้อมูลในช่วงวิกฤต Covid-19 มีวัตถุประสงค์เพื่อศึกษาและวิเคราะห์ปัจจัยที่มีอิทธิพลและส่งผลต่อความไม่สมมาตรของข้อมูลของบริษัทจดทะเบียน ในตลาดหลักทรัพย์แห่งประเทศไทย กลุ่มอุตสาหกรรมบริการทางการแพทย์ และเพื่อทดสอบประสิทธิภาพของแบบประเมินความไม่สมมาตรของข้อมูลในสถานการณ์ที่เปลี่ยนแปลงไปในช่วง covid-19 ว่ายังสามารถทำนายความไม่สมมาตรของข้อมูลที่เกิดขึ้นได้หรือไม่ คณะผู้วิจัยได้เก็บข้อมูลประชากรจากกลุ่มอุตสาหกรรมบริการ กลุ่มย่อยธุรกิจการแพทย์ บริษัทจดทะเบียนในตลาดหลักทรัพย์แห่งประเทศไทย จำนวน 22 บริษัท รอบระยะเวลาบัญชีตั้งแต่ พ.ศ. 2562-2564 รวมทั้งสิ้น 66 บริษัท จำนวน 3 ปี งานวิจัยครั้งนี้ได้ทำการทดสอบความสัมพันธ์ของตัวแปรตามแบบจำลองและแบบประเมินความไม่สมมาตรของข้อมูลในงานวิจัยที่ปรากฎก่อนหน้าของ Kornlert and Sincharoonsak (2022) เพื่อทดสอบว่าตัวแบบพยากรณ์ดังกล่าวยังมีค่าความเชื่อมั่นและสามารถประเมินความไม่สมมาตรของข้อมูลที่เกิดขึ้นได้หรือไม่ ซึ่งผลการทดสอบที่เกิดขึ้นพบว่าตัวแบบพยากรณ์สามารถพยากรณ์การเกิดความไม่สมมาตรของข้อมูลได้แม้อยู่ในช่วงสถานการณ์ความไม่ปกติ COVID–19 และตัวแบบยังให้ความเชื่อมั่นของแบบพยากรณ์ของอิทธิพลทางตรงในระดับร้อยละ 79.30 จากงานวิจัยก่อนหน้าที่ให้ค่าความเชื่อมั่นของอิทธิพลทางตรงและทางอ้อมในระดับร้อยละ 32

เอกสารอ้างอิง

Akerlof, G. .A. (1970). "The market for 'Lemons'. Quality, Uncertainty and Market Mechanism" Quarterly Journal of Economics, Vol. 84(3), 488-500. https://doi.org/10.2307/1879431

Alamdari, N. N. (2016). "Relationship between Information Asymmetry and Dividend Policy of Companies Listed in TSE." International Journal of Arts-based Educational Research. Vol14(10), 7043-7054. https://serialsjournals.com/abstract/54479_ch-57_afra_1.pdf

Alves, H. S. A. (2011). "Corporate Governance Determinants of Voluntary Disclosure and its Effect on Information Asymmetry: An Analysis for Iberian Peninsula Listed Companies." Faculty of Economic. University of Coimbra. 1-401. https://citeseerx.ist.psu.edu/document?repid=rep1&type=pdf&doi=6e806477522ca82797705f7944343b84a058d730

Bhattacharya, N., Ecker, F., Olsson, P. M. and Schipper, K. (2012). "Direct and Mediated Associations among Earnings Quality, Information Asymmetry, and the Cost of Equity." The Accounting Review. Vol. 87(2), 449-482. https://doi.org/10.2308/accr-10200

Brandenburg, W. H. J. M. and Suijs, J. P. M. (2013). "Voluntary Disclosure and Information Asymmetry in the Netherlands." University of Tilburg. 1-31. https://arno.uvt.nl/show.cgi?fid=132112

Cerqueira, A. and Pereira, C. (2015). "Accounting Accruals and Information Asymmetry in Europe." Prague Economic Papers. Vol. 24(6), 638-661. https://doi.org/10.18267/j.pep.528

Fathi, J. (2013). "Corporate Governance and the Level of Financial Disclosure by Tunisian Firm." Journal of Business Studies Quarterly. Vol.4(3), 95-111. https://citeseerx.ist.psu.edu/document?repid=rep1&type=pdf&doi=acccc2c78fd92849f21cc3f31b8e9293fb2c255a

Farber, D. B. (2004). "Restoring Trust After Fraud: Does Corporate Governance Matter?" The Accounting Review. Vol.80(2), 1-41. https://jstor.org/stable/4093068. https://doi.org/10.2308/accr.2005.80.2.539

Gonzalez, J. S. and Meca, E. G. (2013). "Does Corporate Governance Influence Earning Management in Latin American Markets?." Journal of Business Ethics. Vol.121, 419-440. https://doi.org/10.1007/s10551-013-1700-8

Jensen C. Michael. (1986). Agency Costs of Free Cash Flow, Corporate Finance, and Takeovers. The American Economic Review. Vol.76 (2), 323-329. https://jstor.org/stable/1818789

Jensen C. Michael and Mocking H. William. (1976). "Theory of the Firm: Managerial Behavior Agency Costs and Ownership Structure." Journal of Financial Economics. Vol. 3(4), 305-360. https://doi.org/10.1016/0304-405X(76)90026-X

Kornlert, P. and Sincharoonsak, T. (2022). The Research and Development of Information Asymmetry Assessment. International Journal of Economics and Finance Studies. Vol. 14 (3), 227-248. https://doi.org/10.34109/ijefs.20220071

Kornlert, P. and Penvutikul, P. (2022). The Analysis of Causal Influencing on Information Asymmetry of Listed on the Stock Exchange of Thailand. International Journal of eBusiness and eGovernment Studies. Vol.14(3), 99-119. https://doi.org/ 10.34109/ijebeg. 202214185

Kothari, S. P., Leone, A. J., and Wasley, C. E. (2005). Performance Matched Discretionary Accrual Measures. Journal of Accounting and Economics. Vol.39 (1), 163-197. https://doi.org/10.1016/j.jacceco.2004.11.002

Monnakgotla Zanele. (2014). "A Comparative Analysis of the Abnormal Returns Made by Acquirers in Acquisitions on the Johannesburg Securities Exchange South Africa (JSE)." [Master's thesis, University of the Witwatersrand]. Johannesburg. 1-105. https://wiredspace.wits.ac.za/server/api/core/bitstreams/2a9a87ba-e3ef-417a-a933-cec5261a9d17/content

Petersen, C. and Plenborg, T. (2006). "Voluntary Disclosure and Information Asymmetry in Denmark." Journal of International Accounting, Auditing and Taxation. Vol.15 (2), 127-149. https://doi.org/10.1016/j.intaccaudtax.2006.08.004

Palazzo, F. and Zhang, M. (2017). "Information Disclosure and Asymmetric Speed of Learning in Booms and Busts." Economics Letters. Vol.158, 7-40. https://doi.org/10.1016/j.econlet.2017.06.027

Raithatha, M. and Bapat, V. (2014). "Impact of Corporate Governance on Financial Disclosures: Evidence from India." Corporate Ownership and Control. Vol.12 (1), 874-889. https://doi.org/10.22495/cocv12i1c9p10

Sahar, M. E. and Mayahi, N. (2014). "Asymmetric Information and Dividend Payout Policy: Evidence from Iran Stock Exchange." Indian Journal of Fundamental and Applied Life Sciences. Vol.4(1), 30-35. https://cibtech.org/sp.ed/jls/2014/01/00(4).pdf

Shroff, N., Sun, A. X.,White, H. D. and Zhang, W. (2013). "Voluntary Disclosure and Information Asymmetry: Evidence from the 2005 Securities Offering Reform." Journal of Accounting Research. Vol.51(5), 1299-1345. https://doi.org/10.1111/1475-679X.12022

Securities and Exchange Commission. (2015). Corporate Governance Policy of the Stock Exchange of Thailand Group. Retrieved December 30, 2023, https://www.set.or.th/th/about/overview/cg

Wang, Q., Wong, T. J. and Xia, L. (2008). "State Ownership, The Institutional Environment, and Auditor Choice: Evidence Form China." Journal of Accounting and Economics. Vol.46 pp. 112-134. https://doi.org/10.1016/j.jacceco.2008.04.001

Ziabari, A. Z., Samadi, M., Meshki, M. and Masouleh, H. P. (2014). "Study of the Relationship between Information Asymmetry and Cash Dividend Policy." Management and Administrative Sciences Review. Vol.3(4), pp. 615-623.

ดาวน์โหลด

เผยแพร่แล้ว

รูปแบบการอ้างอิง

ฉบับ

ประเภทบทความ

สัญญาอนุญาต

ลิขสิทธิ์ (c) 2024 คณะบริหารธุรกิจ สถาบันบัณฑิตพัฒนบริหารศาสตร์

อนุญาตภายใต้เงื่อนไข Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.