ผลการดำเนินงานของกองทุนรวมหุ้นไทยในช่วงวิกฤตการณ์ Covid-19

คำสำคัญ:

กองทุนรวมหุ้นไทย, วิกฤติการณ์โควิด, การลงทุนแบบเชิงรุก, ค่าอัลฟ่า, สภาวะเศรษฐกิจหดตัวบทคัดย่อ

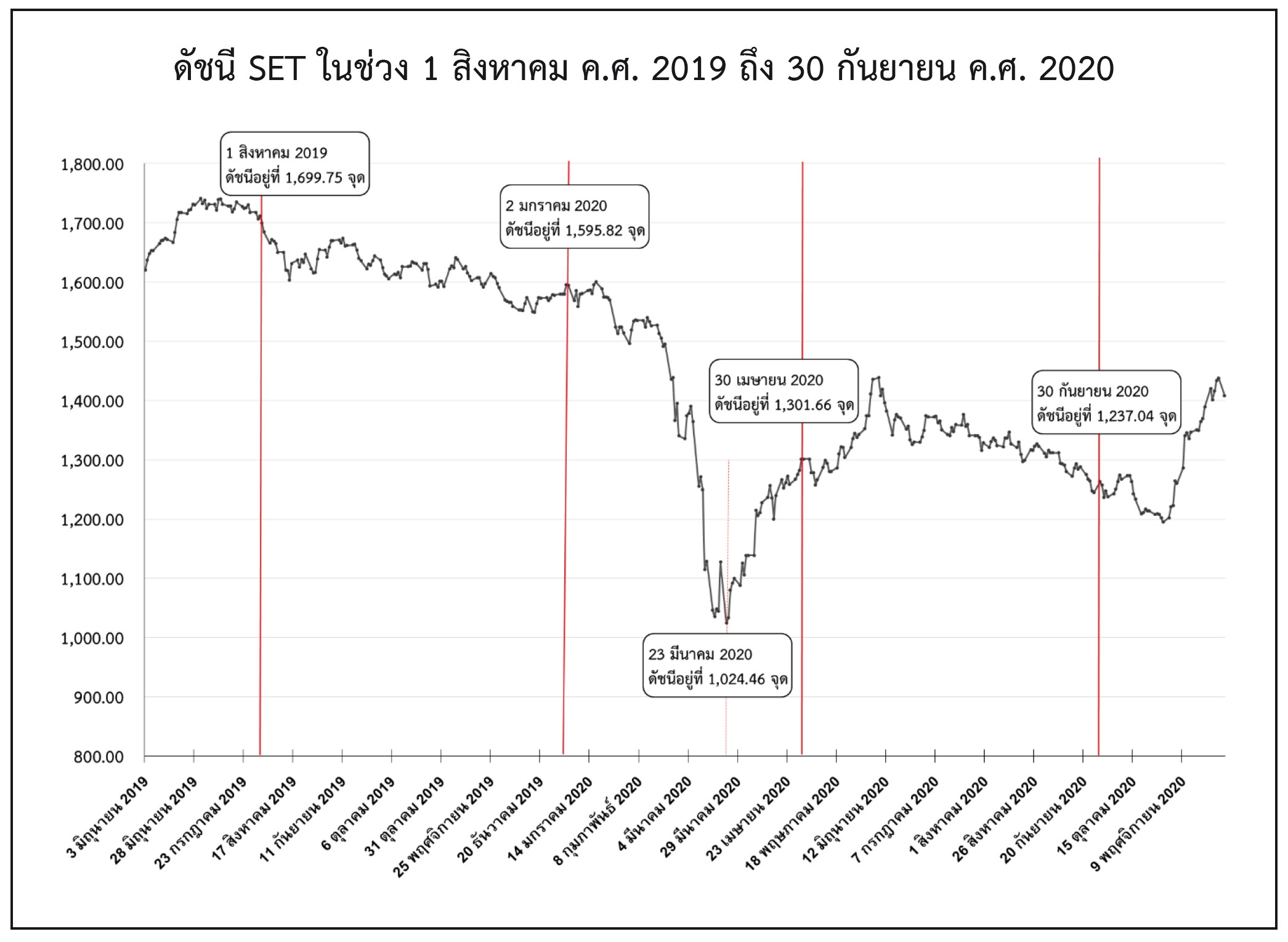

งานวิจัยนี้ประเมินผลการดำเนินงานของกองทุนรวมหุ้นไทยที่มีนโยบายลงทุนเชิงรุกจำนวน 274 กองทุนในช่วงวิกฤติการณ์โควิด ผลการศึกษาพบว่า ในช่วงวิกฤตโควิดที่หุ้นมีการปรับลงรุนแรงและผันผวนและเป็นช่วงที่ภาวะเศรษฐกิจชะลอตัว ตั้งแต่ 2 มกราคม ค.ศ. 2020 ถึง 30 เมษายน ค.ศ. 2020 กองทุนรวมหุ้นไทยทำผลตอบแทนโดยเฉลี่ยได้ต่ำกว่าตลาดถึง -3.86% ต่อปี และทำค่าอัลฟ่าจากแบบจำลอง CAPM (Capital Asset Pricing Model) ติดลบถึง -6.87% ต่อปี ซึ่งไม่สอดคล้องกับผลการศึกษาเชิงประจักษ์ในต่างประเทศที่พบว่า แม้กองทุนรวมหุ้นมักทำผลตอบแทนโดยเฉลี่ยในทุกสถานการณ์ที่ต่ำกว่าผลตอบแทนตลาด แต่มาทำผลตอบแทนที่เหนือกว่าตลาดได้ในช่วงเศรษฐกิจหดตัว และไม่สอดคล้องกับสมมุติฐานของ Glode (2011) ที่ว่ากองทุนรวมหุ้นมาทำผลตอบแทนได้ดีกว่ามาตรฐานในช่วงเศรษฐกิจหดตัว เพื่อเป็นการป้องกันความเสี่ยงให้กับนักลงทุน เพราะในช่วงเศรษฐกิจหดตัว อรรถประโยชน์ส่วนเพิ่มของนักลงทุนจะสูงขึ้น

เอกสารอ้างอิง

Banegas, A., Gillen, B., Timmermann, A., & Wermers, R. (2013). The Cross Section of Conditional Mutual Fund Performance in European Stock Markets. Journal of Financial Economics, 108(3), 699-726. https://doi.org/10.1016/j.jfineco.2013.01.008

Carhart, M. M. (1997). On Persistence in Mutual Fund Performance. The Journal of Finance, 52(1), 57-82. https://doi.org/10.1111/j.1540-6261.1997.tb03808.x

Fama, E. F., & French, K. R. (2010). Luck Versus Skill in the Cross-Section of Mutual Fund Returns. The Journal of Finance, 65(5), 1915-1947, https://doi.org/10.1111/j.1540-6261.2010.01598.x

Glode, V. (2011). Why Mutual Funds Underperform? Journal of Financial Economics, 99(3), 546-559. https://doi.org/10.1016/j.jfineco.2010.10.008

Jensen, M. (1968). The Performance of Mutual Fund in the Period 1945-1964. Journal of Finance, 23(2), 389-416. https://doi.org/10.1111/j.1540-6261.1968.tb00815.x

Jenwittayaroje, N. (2017). The Performance and Its Persistence of Thailand Equity Mutual Funds from 1995-2014. Chulalongkorn Business Review, Vol. 39 Issue 152, page 57-89.

Jenwittayaroje, N. (2018). Returns and Their Persistence from Investing in Active Long-Term Equity Funds and Active Equity Retirement Funds. NIDA Business Journal, Vol. 22, page 61-86.

Kosowski, R. (2011). Do Mutual Funds Perform When It Matters Most to Investors? US Mutual Fund Performance and Risk in Recessions and Expansions. Quarterly Journal of Finance, 1(3), 607-664. https://doi.org/10.1142/S2010139211000146

Malkiel, B. G. (1995). Returns from Investing in Equity Mutual Funds 1971 to 1991. The Journal of Finance, 50(2), 549-572. https://doi.org/10.1111/j.1540-6261.1995.tb04795.x

Moskowitz, T. J. (2000). Mutual Fund Performance: An Empirical Decomposition into Stock-Picking Talent, Style, Transactions Costs, and Expenses: Discussion. Journal of Finance 55, 1695-1703. https://doi.org/10.1111/0022-1082.00264

Pástor, L., and M. B. Vorsatz. (2020). Mutual Fund Performance and Flows During the COVID-19 Crisis. The Review of Asset Pricing Studies, 10(4), 791-833. https://doi.org/10.1093/rapstu/raaa015

Wermers, R. (2000). Mutual Fund Performance: An Empirical Decomposition into Stock-Picking Talent, Style, Transactions Costs, and Expenses. The Journal of Finance, 55(4), 1655-1695. https://doi.org/10.1111/0022-1082.00263

ดาวน์โหลด

เผยแพร่แล้ว

รูปแบบการอ้างอิง

ฉบับ

ประเภทบทความ

สัญญาอนุญาต

ลิขสิทธิ์ (c) 2023 คณะบริหารธุรกิจ สถาบันบัณฑิตพัฒนบริหารศาสตร์

อนุญาตภายใต้เงื่อนไข Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.