การศึกษาความสามารถในการทำกำไรในทางปฏิบัติของกลยุทธ์ “การขายหุ้นในเดือนพฤษภาคม” ในตลาดหลักทรัพย์แห่งประเทศไทย

บทคัดย่อ

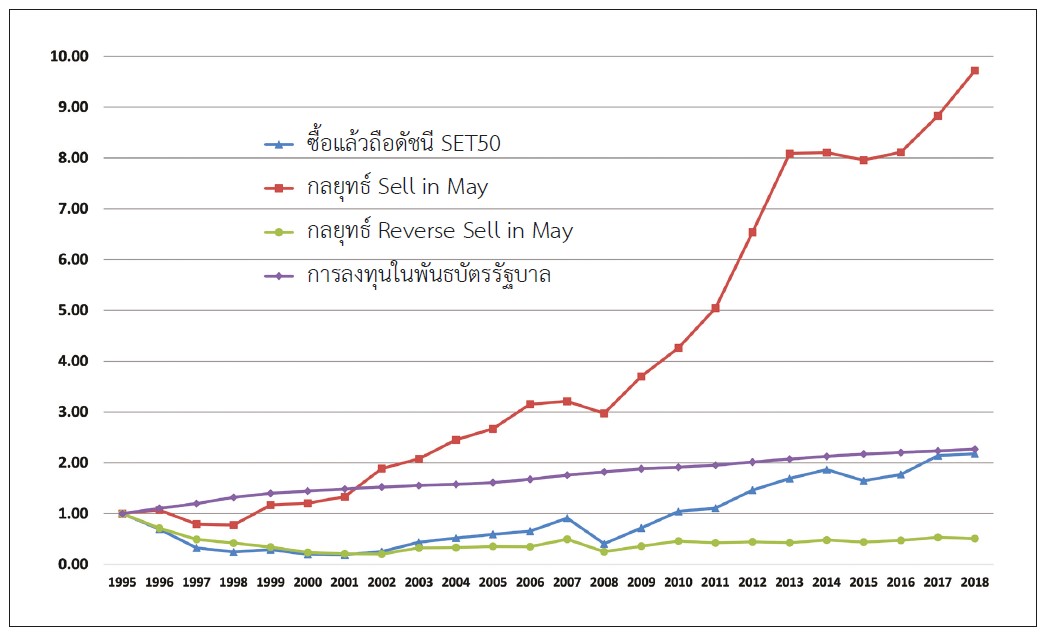

งานวิจัยนี้ได้ทดสอบความสามารถในการทำกำไรในทางปฏิบัติของกลยุทธ์ “Sell in May and Go Away” (หรือกลยุทธ์ Sell in May) ของดัชนี SET50 ของตลาดหลักทรัพย์แห่งประเทศไทยในช่วงปี 1995-2018 โดยพบหลักฐานเชิงประจักษ์ของปรากฏการณ์ Sell in May ในช่วงเวลาดังกล่าวที่สอดคล้องกับ Bouman and Jacobsen (2002) และณัฐวุฒิ (2560) โดยพบว่าผลตอบแทนรวมเฉลี่ยของดัชนี SET50 ในช่วงเดือน พ.ค. ถึง ต.ค. นั้นมีค่า -1.36% แต่ในช่วงเดือน พ.ย. ถึง เม.ย. นั้นสูงถึง 9.74% ต่อ 6 เดือน นอกจากนี้ การศึกษานี้ได้ทำการทดสอบความสามารถในการทำกำไรในทางปฏิบัติของกลยุทธ์ Sell in May โดยใช้กองทุน TDEX ในช่วงปี 2007-2018 และสัญญาซื้อขายล่วงหน้าบนดัชนี SET50 (SET50 Index Futures) ในช่วงปี 2006-2018 เป็นตัวแทนของการลงทุนในดัชนี SET50 และเพื่อใช้อัตราทด (Leverage) ของตราสาร SET50 Index Futures ประกอบการลงทุน และพบหลักฐานเชิงประจักษ์ที่แสดงให้เห็นว่ากลยุทธ์ Sell in May ในทางปฏิบัติเหล่านี้สามารถทำผลตอบแทนเฉลี่ยที่เหนือกว่าผลตอบแทนของการซื้อแล้วถือ (Buy and Hold) กองทุน TDEX ทั้งปี และมีค่าความเสี่ยงที่วัดด้วยค่าเบี่ยงเบนมาตรฐาน (Standard Deviation) และค่าเบต้าที่ต่ำกว่าการลงทุนแบบซื้อแล้วถือกองทุน TDEX อย่างมาก จึงทำให้กลยุทธ์ Sell in May โดยใช้กองทุน TDEX และ SET50 Index Futures สามารถทำค่าแอลฟ่า (Jensen’s Alpha) ได้สูงถึง 0.2% ถึง 5.7% ต่อ 6 เดือนหรือประมาณ 0.4% ถึง 11.4% ต่อปีทีเดียว

เอกสารอ้างอิง

Jenwittayaroje, N. (2017). "The study of "Sell in May" in the Stock Exchange of Thailand". NIDA Business Journal, Vol. 20 (May), pp 117-132.

Andrade, S.C., Chhaochharia, V., & Fuerst, M. E. (2013). "Sell in May and Go Away" just won't go away. Financial Analysts Journal 69(4), 94-105. https://doi.org/10.2469/faj.v69.n4.4

Bouman, S., & Jacobsen, B. (2002). The Halloween indicator, "Sell in May and Go Away": Another puzzle. American Economic Review 92(5), 1618-1635. https://doi.org/10.1257/000282802762024683

Dichtl, H., & Drobetz, W. (2015). Sell in May and go away: still good advice for investors? International Review of Financial Analysis 38, 29-43. https://doi.org/10.1016/j.irfa.2014.09.007

Haggard, K.S., & Witte, H.D. (2010). The Halloween effect: trick or treat? International Review of Financial Analysis 19, 379-387. https://doi.org/10.1016/j.irfa.2010.10.001

Haggard, K.S., Jones, J.S., & Witte, H.D. (2015). Black cats or black swans? Outliers, seasonality in return distribution properties, and the Halloween effect. Managerial Finance 41(7), 642-657. https://doi.org/10.1108/MF-07-2014-0190

Jacobsen, B., & Visaltanachoti, N. (2009). The Halloween effect in U.S. sectors. The Financial Review 44(3), 437-459. https://doi.org/10.1111/j.1540-6288.2009.00224.x

Jacobsen, B., & Zhang, C.Y. (2018). The Halloween indicator, "sell in May and go away": everywhere and all the time. Working paper, Massey University.

Jones, C.P., & Lundstrum, L.L. (2009). Is "Sell in May and Go Away" a valid strategy for U.S. equity allocation? Journal of Wealth Management 12(3), 104-112. https://doi.org/10.3905/jwm.2009.12.3.104

Maberly, E.D., & Pierce, R.M. (2004). Stock market efficiency withstands another challenge: Solving the "Sell in May/Buy after Halloween" puzzle. Econ Journal Watch 1(1), 29-46.

Witte, H.D. (2010). Outliers and the Halloween Effect: comment on Maberly and Pierce. Econ Journal Watch 7(1), 91-98.

ดาวน์โหลด

เผยแพร่แล้ว

รูปแบบการอ้างอิง

ฉบับ

ประเภทบทความ

สัญญาอนุญาต

ลิขสิทธิ์ (c) 2019 https://creativecommons.org/licenses/by-nc-nd/4.0/

อนุญาตภายใต้เงื่อนไข Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.