การจัดการกำไรผ่านรายการคงค้างในดุลยพินิจของฝ่ายบริหารของบริษัทจดทะเบียนที่อยู่ระหว่างฟื้นฟูการดำเนินงานในตลาดหลักทรัพย์แห่งประเทศไทย

คำสำคัญ:

การจัดการกำไร, รายการคงค้างในดุลยพินิจของฝ่ายบริหาร, บริษัทจดทะเบียนที่อยู่ระหว่างฟื้นฟูการดำเนินงาน, Modified Jones Model (1995)บทคัดย่อ

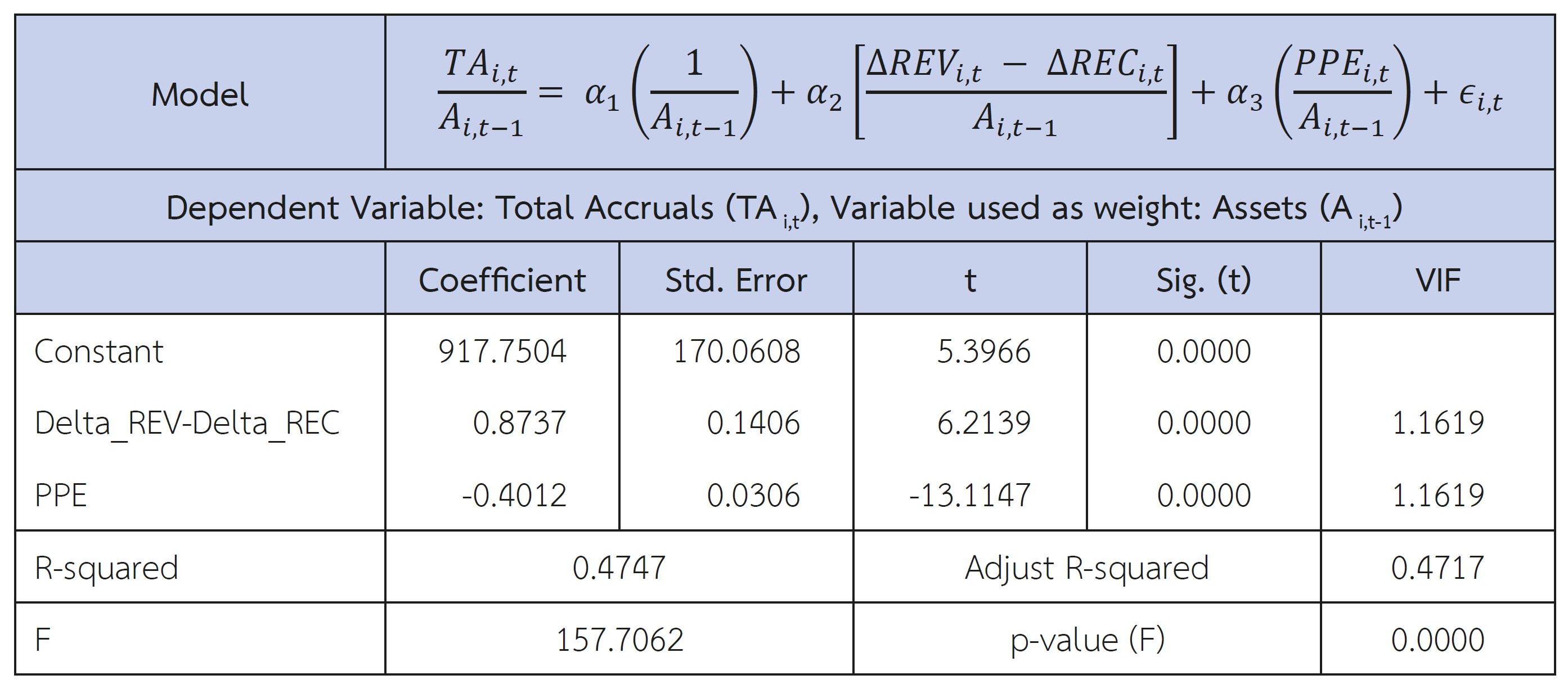

การศึกษานี้มีวัตถุประสงค์เพื่อศึกษาแนวโน้มและขนาดของการจัดการกำไร ตลอดจนปัจจัยที่มีผลต่อการจัดการกำไรโดยผ่านรายการคงค้างในดุลยพินิจของฝ่ายบริหารของบริษัทจดทะเบียนที่อยู่ระหว่างฟื้นฟูการดำเนินงานตามแบบจำลองการจัดการกำไร Modified Jones Model (1995) ในช่วงปี พ.ศ. 2554 ถึง พ.ศ. 2559 เปรียบเทียบกับบริษัทจดทะเบียนที่อยู่ในสถานะปกติซึ่งมีขนาดของสินทรัพย์เฉลี่ยใกล้เคียงกันและอยู่ในอุตสาหกรรมเดียวกัน จำนวน 44 บริษัท 264 ข้อมูล โดยใช้การทดสอบทางสถิติแบบจับคู่เปรียบเทียบค่าเฉลี่ยระหว่างกลุ่มรวมทั้งเทคนิคการวิเคราะห์ความถดถอยเชิงพหุ

ผลการศึกษาพบว่า การจัดการกำไรของบริษัทจดทะเบียนในช่วงฟื้นฟูการดำเนินงานมีแนวโน้มเพิ่มขึ้นในลักษณะรายการคงค้างในดุลยพินิจของฝ่ายบริหารเป็นลบ และมีขนาดของการจัดการกำไรมากกว่าบริษัทจดทะเบียนที่อยู่ในสถานะปกติอย่างมีนัยสำคัญทางสถิติ นอกจากนี้ ยังพบว่า ณ ระดับความเชื่อมั่น 95% บริษัทที่อยู่ในสถานะฟื้นฟูกิจการมีความสัมพันธ์กับการจัดการกำไรเชิงบวก และปัจจัยที่มีผลต่อการจัดการกำไรของบริษัทจดทะเบียนที่อยู่ระหว่างฟื้นฟูการดำเนินงาน ได้แก่ อัตราส่วนผลตอบแทนต่อสินทรัพย์รวมและขนาดของกิจการ โดยมีความสัมพันธ์เชิงบวก ส่วนกระแสเงินสดจากการดำเนินงาน ขนาดของสำนักงานสอบบัญชี และกำไรจากการปรับโครงสร้างหนี้ มีความสัมพันธ์ในทิศทางตรงกันข้ามกับการจัดการกำไร

เอกสารอ้างอิง

Aharony, J., Lin, C. J., & Loeb, M. P. (1993). Initial Public Offerings, Accounting Choices and Earnings Management. Contemporary Accounting Research, 10(1), 61-81.

Ahmed, R.B. (2004). Accounting Theory. 5th ed. United Kingdom: Thomson.

Ajit, D., Sarat, M., & Vimal, K.V. (2013). Earning Management in India. SEBI DRG Study, 1 – 27. Retrieved June 20, 2014 from http://www.sebi.gov.in/cms/sebi_data/DRG_Study/EMiM.pdf.

Aroonjit, W. (2005). The Relationship between Audit Firm Size, Firm Size and Earnings Management: Case of Listed Companies in the Stock Exchange of Thailand. Thesis of Master of Accountancy Program, Chulalongkorn University.

Awidat, M., & Vladan, P. (2013). Earning Management vs Financial Reporting Fraud Key Features for Distinguishing. Economics and Organization, 10(1), 39-47.

Bartov, E., Gul, F. A., & Tsui, J.S.L. (2000). Discretionary-Accruals Models and Audit Qualifications. Journal of Accounting and Economics, 30(3), 421-452.

Bauwhede, H.V., Marleen, W., & Gaeremynck, A. (2003). Audit Firm Size Public Ownership, and Firms' Discretionary Accruals Management. The International Journal of Accounting, 38, 1-22.

Bergstresser, D., & Philippon, T. (2006). CEO Incentives and Earnings Management. Journal of Financial Economics, 80, 511–529.

Cheng, Q., Warfield, T., & Ye, M. (2005). Equity Incentives and Earnings Management. The Accounting Review, 80, 441-476.

Dechow, P. M., Sloan, R. G., & Sweeney, A. P. (1995). Detecting Earnings Management. The Accounting Review. 70: 193-225.

Elias, S., Jamal, B. K., & Mohammad, H. (2013). The Study of Relationship between Annual Adjustments in Financial Statements and Earning Management. Interdisciplinary Journal of Contemporary Research in Business, 5(4), 275 - 283.

Essam, E., & Emmanuel, N. (2014). Are Discretionary Accruals a Good Measure of Audit Quality?. Journal of Management Policy and Practice, 15(2), 43-59.

Guay, W., S. P. Kothari, & R.L. Watts. (1996). A Market-Based Evaluation of Discretionary Accruals Model. Journal of Accounting Research, 34, 83-105.

Hashem, N., Bahman, B., & Azam, S. (2012). An Empirical Analysis of Earnings Management Motives in Firms Listed on Tehran Stock Exchange. Journal of Basic and Applied Scientific Research, 2(10), 9990 – 9993.

Healy, P.M., & Wahlen, J. M. (1999). A Review of the Earnings Management Literature and Its Implications for Standard Setting. Accounting Horizons, 13(4), 365-383.

Jaggi, B. & Lee, P. (2002). Earnings Management Response to Debt Covenants and Debt Restructuring. Journal of Accounting, Auditing & Finance, 17, 295-324.

Jiang, J., Petroni, K.R., & Wang, I.Y. (2010). CFOs and CEOs: Who Have the Most Influence on Earnings Management?. Journal of Financial Economics, 96, 513-526.

Kampanatkoson, K. (2007). Earnings Management and Leverage Ratio. Independent Study of Master of Accounting Program, Thammasat University.

Kate, J. (2007). The Effect of Leverage Increases on Earning Management. Journal of Business & Economic Studies, 13(2), 24-46.

Komkhuntod, S. (2012). Factors that Affect Earnings Management through Accruals of Companies Listed on the Stock Exchange of Thailand, Which was ordered to edit the Financial Statements. Thesis of Master of Accountancy Program, Khon Kaen University.

Maneemai, P., & Sriworadetpisan, S. (2009). Earnings Management of Financial Distressed Firms during Debt Restructuring Negotiation. Academic Journal of University of the Thai Chamber of Commerce, 29(4), 1-21.

Merchant, K. A., & Rockness, J. (1994). The Ethics of Managing Earnings: an Empirical Investigation. Journal of Accounting and Public Polky, 13(1), 79-94.

Peasnell, K., Popoe, P., & Young, S. (2000). Accrual Management to Meet Earnings Targets: UK Evidence Pre-and Post-Cadbury. British Accounting Review, 32, 415-445.

Park, M. S., & Ro, B. T. (2004). The Effect of Firm-Industry Earning Correlation and Announcement Timing on Firm's Accrual Dicision. The British Accounting Review, 36, 269-289.

Pratomsrimek, S. (2005). Factor Leading to the Success in Rehabilitation Process: An Empirical Evidence from the Stock Exchange of Thailand. Ph.D. Dissertation, Department of Accountancy, Chulalongkron University.

Richardson, S. A., Sloan, S. G., Soliman, M., & Tuna, I. (2005). Accrual Reliability Earnings Persistence and Stock Prices. Journal of Accounting and Economics, 39, 437-485.

Ronen, J., & Yaari, V. (2008). Earnings Management: Emerging Insights in Theory, Practice and Research. New York: Springer Science and Business Media.

Schipper, K. (1989). Earnings Management. Accounting Horizons, 3 (4), 91-102.

Sundod, J. (2005). The Relationship between Financial Performances and Accounting Accruals. Thesis of Master of Accountancy Program, Chulalongkorn University.

Sylvia, V.S., & Sidharta, U. (2008). Type of Earning Management and the Effect of Ownership Structure, Firm Size, and Corporate-Governance Practices: Evidence from Indonesia. The International Journal of Accounting, 43, 1-27.

TanTana, P. (2011). Earnings Management by Accruals of Initial Public Offering Firms in the Stock Exchange of Thailand. Thesis of Master of Accountancy Program, Kasetsart University.

Tummanon, V. (2000). Did you know Creative Accounting and Earning Quality?. Ionic Inter Trade Resources, Bangkok.

ดาวน์โหลด

เผยแพร่แล้ว

รูปแบบการอ้างอิง

ฉบับ

ประเภทบทความ

สัญญาอนุญาต

ลิขสิทธิ์ (c) 2020 https://creativecommons.org/licenses/by-nc-nd/4.0/

อนุญาตภายใต้เงื่อนไข Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.