ผลกระทบของคณะกรรมการทับซ้อนที่มีต่อมูลค่าเพิ่มทางการตลาดของ บริษัทที่จดทะเบียนในตลาดหลักทรัพย์แห่งประเทศไทย: การถือหุ้นของผู้บริหารในฐานะตัวแปรกำกับ

คำสำคัญ:

กรรมการทับซ้อน, มูลค่าเพิ่มทางการตลาด, การถือหุ้นของผู้บริหาร, ตลาดหลักทรัพย์แห่งประเทศไทยบทคัดย่อ

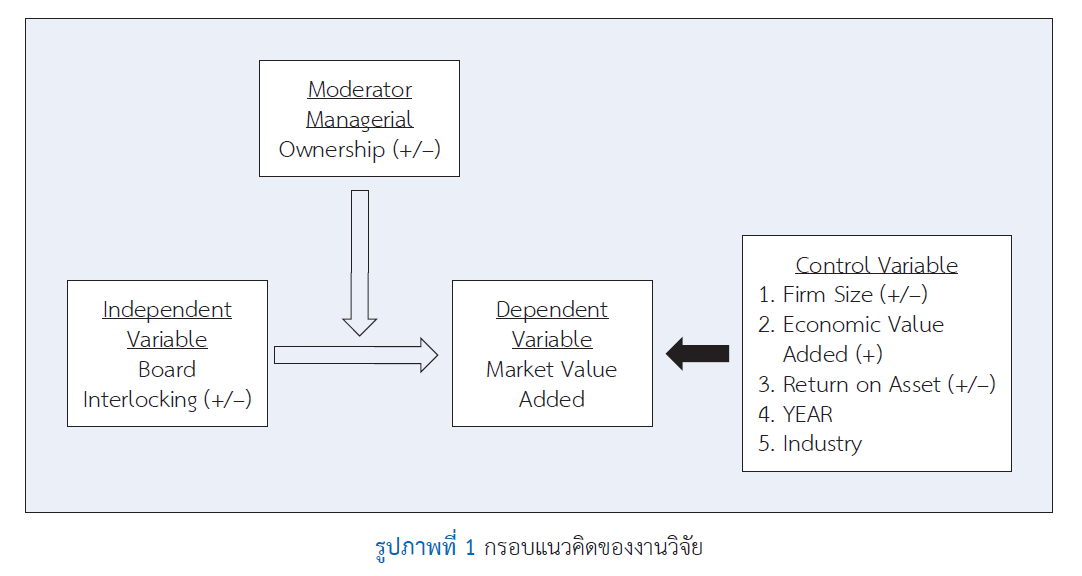

การศึกษานี้มุ่งเน้นเพื่อทดสอบผลกระทบของกรรมการทับซ้อนที่มีต่อมูลค่าเพิ่มทางการตลาดโดยมีสัดส่วนการถือหุ้นของผู้บริหารเป็นตัวแปรกำกับ การศึกษานี้ใช้กลุ่มตัวอย่างจากบริษัทจดทะเบียนในตลาดหลักทรัพย์แห่งประเทศไทย ตั้งแต่ปี 2564 ถึง 2566 จำนวนทั้งสิ้น 1,350 ตัวอย่าง จาก 450 บริษัท

การวิเคราะห์ข้อมูลใช้ทั้งสถิติเชิงพรรณนาและสถิติเชิงอนุมาน และจากการใช้แบบจำลองของสมการถดถอยเชิงพหุคูณแบบรวมภาคตัดขวาง (Pooled OLS Regression)

ผลการศึกษาพบว่ากรรมการทับซ้อนมีความสัมพันธ์เชิงบวกกับมูลค่าเพิ่มทางการตลาดอย่างมีนัยสำคัญทางสถิติที่ระดับ 5% สะท้อนว่าการที่กรรมการดำรงตำแหน่งในหลายบริษัทช่วยเพิ่มมูลค่าทางการตลาดได้อย่างมีนัยสำคัญซึ่งสอดคล้องกับทฤษฎีการพึ่งพิงทรัพยากร (Resource Dependence Theory) อีกทั้งผลการศึกษานี้ยังชี้ให้เห็นว่าสัดส่วนการถือหุ้นของผู้บริหารมีผลกระทบต่อความสัมพันธ์ของกรรมการทับซ้อนกับมูลค่าเพิ่มทางการตลาดในเชิงลบอย่างมีนัยสำคัญทางสถิติที่ระดับ 5% กล่าวได้ว่าเมื่อสัดส่วนการถือหุ้นของผู้บริหารเพิ่มขึ้นบทบาทของกรรมการทับซ้อนที่ช่วยเพิ่มมูลค่าทางการตลาดให้กับบริษัทจะลดลง ซึ่งสอดคล้องกับทฤษฎีตัวแทนที่ชี้ให้เห็นถึงความเสี่ยงของพฤติกรรมของผู้บริหารที่ไม่สอดคล้องกับผลประโยชน์ของผู้ถือหุ้น นอกจากนี้ยังพบว่าขนาดของบริษัทมีความสัมพันธ์เชิงลบกับมูลค่าเพิ่มทางการตลาด ในทางตรงข้ามผลตอบแทนจากสินทรัพย์มีความสัมพันธ์เชิงบวกกับมูลค่าเพิ่มทางการตลาด

เอกสารอ้างอิง

Adsakul, N. (2015). Performance measures affecting economic value added and market value added of company in services industry group in the Stock Exchange of Thailand [Master’s thesis, Sripatum University].

Biswas, S., Sarkar, J., & Selarka, E. (2023). Women director interlocks and firm performance: Evidence from India (Working Paper No. WP-2023-016). Indira Gandhi Institute of Development Research. https://doi.org/10.2139/ssrn.4653412

Dal Vesco, D. G., & Beuren, I. M. (2016). Do the board of directors composition and the board interlocking influence on performance? BAR-Brazilian Administration Review, 13(2) Article 1, e160007. http://dx.doi.org/10.1590/1807-7692bar2016160007

Dawson, J. F. (2013). Moderation in management Research: What, why, when, and how. Journal of Business and Psychology, 29(1), 1-19. https://doi.org/10.1007/s10869-013-9308-7

Dee-Arsa, P., & Sittipatna, P. (2024). The relevance of economic value added and financial performance measures on the market value added of companies in the sustainable stock price movement index group list in the Stock Exchange of Thailand. Western University Research Journal of Humanities and Social Science, 10(1), 113-126.

Drucker, P. (1993). Post-capitalist society. Butterworth-Heinemann.

Edacherian, S., Richter, A., Karna, A., & Gopalakrishnan, B. (2023). Connecting the right knots: The impact of board committee interlocks on the performance of Indian firms. Corporate Governance an International Review, 32(1), 135-155. https://doi.org/10.1111/corg.12523

Farwis, M., & Nazar, M. C. A. (2019). Interlocking directorate and firm performance of listed companies in Sri Lanka. Asian Journal of Research in Banking and Finance, 9(3), 1-15. https://doi.org/10.5958/2249-7323.2019.00003.8

Gujarati, D. N., & Porter, D. C. (2009). Basic econometrics (5th ed.). McGraw-Hill Education.

Hamdan, A. (2018). Board interlocking and firm performance: The role of foreign ownership in Saudi Arabia. International Journal of Managerial Finance, 14(3), 266-281. https://doi.org/10.1108/IJMF-09-2017-0192

Haunschild, P., & Beckman, C. (1998). When do interlocks matter? Alternate sources of information and interlock influence. Administrative Science Quarterly, 43(4), 815-845. https://doi.org/10.2307/2393617

Ifada, L. M., Fuad, K., & Kartikasari, L. (2021). Managerial ownership and firm value: The role of corporate social responsibility. Jurnal Akuntansi dan Auditing Indonesia, 25(2), 162-171. https://doi.org/10.20885/jaai.vol25.iss2.art6

Jensen, M. C., & Meckling, W. H. (1976). Theory of the firm: Managerial behavior, agency costs and ownership structure. Journal of Financial Economics, 3(4), 305-360. https://doi.org/10.1016/0304-405X(76)90026-X

Jetiya, A., Kawewong, N., & Diskulnetivitya, P. (2022). Impact of economic value added and financial ratios towards market value added of listed companies in SET100 Index. Journal of Administrative and Management Innovation, 10(1), 24-33.

Morck, R., Shleifer, A., & Vishny, R. W. (1988). Management ownership and market valuation: An empirical analysis. Journal of Financial Economics, 20, 293-315. https://doi.org/10.1016/0304-405X(88)90048-7

Park, J. H. (2025). The impact of interlocking directorates on firm value: Empirical evidence from KOSDAQ companies in Korea. Global Business & Finance Review, 30(1), 100-115. https://doi.org/10.17549/gbfr.2025.30.1.100

Peng, M. W., Mutlu, C. C., Sauerwald, S., Au, K. Y., & Wang, D. Y. L. (2015). Board interlocks and corporate performance among firms listed abroad. Journal of Management History, 21(2), 257-282. https://doi.org/10.1108/JMH-08-2014-0132

Pfeffer, J., & Salancik, G. R. (1978). The external control of organizations: A resource dependence approach. Harper and Row Publishers.

Sany, C., Novica, C., & Valentina, C. (2024). Do board multiple directorships and ESG score drive firm value? Study of non-financial companies in Thailand. Jurnal Akuntansi dan Keuangan, 26(1), 67–76. https://doi.org/10.9744/jak.26.1.67-76

Srivardhana, T. (2010). The effects of board interlocking networks: A case study of listed companies in the Stock Exchange of Thailand [Master’s thesis, National Institute of Development Administration].

Stewart, G. B. (1991). The quest for value. Harper Business.

Sukeecheep, S., Yarram, S. R., & Al Farooque, O. (2013, March 20–23). Earnings management and board characteristics in Thai listed companies. The 2013 IBEA International Conference on Business, Economics, and Accounting, Bangkok, Thailand.

Tan, K. M., Bany-Ariffin, A. N., Kamarudin, F., & Abdul Rahim, N. (2019). Does directors’ experience positively moderate the impact of board busyness on firm efficiency? Evidence from Asia-Pacific. Asia-Pacific Journal of Business Administration, 11(3), 232- 250. https://doi.org/10.1108/APJBA-01-2019-0008

The Stock Exchange of Thailand. (2017). Corporate governance code for listed companies. The Stock Exchange of Thailand.

Ullah, W., Ali, S., & Mehmood, S. (2017). Impact of excess control, ownership structure and corporate governance on firm performance of diversified group firms in Pakistan. Business & Economic Review, 9(2), 49–72. https://doi.org/10.22547/BER/9.2.3

Venkatesh, G., Kshatriya, S., & Bansal, S. (2024). Board busyness and firm performance: An emerging market perspective. Corporate Governance: An International Review, 33(2), 231-245. https://doi.org/10.1111/corg.12600

Young, S. D., & O’Byrne, S. F. (2001). EVA and value based management. McGraw Hill.

ดาวน์โหลด

เผยแพร่แล้ว

รูปแบบการอ้างอิง

ฉบับ

ประเภทบทความ

สัญญาอนุญาต

ลิขสิทธิ์ (c) 2025 คณะบริหารธุรกิจ สถาบันบัณฑิตพัฒนบริหารศาสตร์

อนุญาตภายใต้เงื่อนไข Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.