อุปสรรคและปัจจัยสนับสนุนต่อการยอมรับระบบภาษีอิเล็กทรอนิกส์ (e-Tax): กรณีศึกษาเชิงปริมาณจากประเทศไทย

คำสำคัญ:

ใบกำกับภาษีอิเล็กทรอนิกส์, การออกใบกำกับภาษีด้วยระบบอิเล็กทรอนิกส์, ระบบใบกำกับภาษีอิเล็กทรอนิกส์, ใบกำกับภาษีอิเล็กทรอนิกส์ผ่านอีเมลบทคัดย่อ

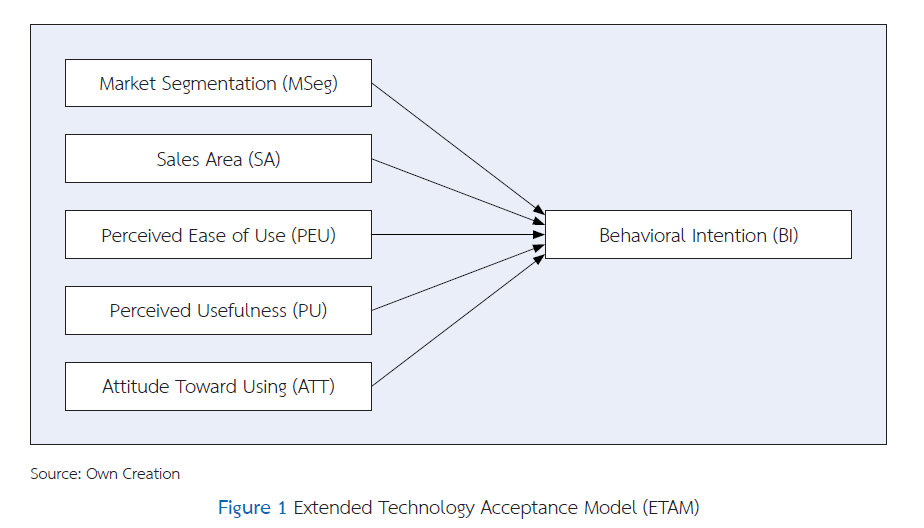

งานวิจัยเชิงปริมาณแบบกรณีศึกษานี้ตรวจสอบปัจจัยที่มีอิทธิพลต่อการยอมรับช่องทาง e-Tax Invoice ทางอีเมลของลูกค้าบริษัท XYZ ซึ่งเป็นบริษัทไทยเพียงรายเดียวที่ศึกษา การเก็บข้อมูลจากลูกค้า 251 ราย ในห้าพื้นที่ขายทั่วประเทศและการวิเคราะห์ด้วยการถดถอยพหุคูณและ ANOVA ทางเดียว พบว่าการรับรู้ประโยชน์ (β = .19, p = .001 การรับรู้ความง่ายในการใช้ (β = .21, p = .001) และทัศนคติต่อการใช้ (β = .54, p < .001) มีอิทธิพลเชิงบวกต่อความตั้งใจใช้ โดยอธิบายความแปรปรวนได้ 49 เปอร์เซ็นต์ การทดสอบ Tukey แสดงว่าลูกค้าในกรุงเทพฯ และปริมณฑล ภาคกลาง และภาคตะวันออกมีคะแนนความตั้งใจใช้สูงกว่าภาคเหนือและภาคตะวันออกเฉียงเหนือ (p < .001) สะท้อนความเหลื่อมล้ำด้านโครงสร้างพื้นฐานดิจิทัลซึ่งเป็นอุปสรรคของการปรับใช้ ปัจจัยความสำเร็จคือการเชื่อมต่อระบบกับซอฟต์แวร์บัญชีอย่างราบรื่น ขั้นตอนเริ่มต้นที่ไม่ซับซ้อน และทัศนคติเชิงบวกของผู้ใช้ ส่วนโครงสร้างพื้นฐานอินเทอร์เน็ตที่อ่อนในภาคเหนือและภาคตะวันออกเฉียงเหนือยังเป็นความท้าทาย ข้อเสนอแนะได้แก่การจัดแพ็กเกจใบรับรองดิจิทัลพร้อมการเริ่มใช้งานและความร่วมมือกับผู้ให้บริการอินเทอร์เน็ตในภูมิภาค ผลลัพธ์ให้บทเรียนที่ขยายผลได้สำหรับ SME ไทยที่วางแผนปรับใช้ e-Tax ในลักษณะเดียวกัน

เอกสารอ้างอิง

Ajzen, I., & Fishbein, M. (2000). Attitudes and the attitude-behavior relation: Reasoned and automatic processes. European Review of Social Psychology, 11(1), 1–33. https://doi.org/10.1080/14792779943000116

Brislin, R. W. (1986). The wording and translation of research instruments. In W. J. Lonner & J. W. Berry (Eds.), Field Methods in Cross-Cultural Research (pp. 137–164). Sage Publications.

Chakpitak, N., Maneejuk, P., Chanaim, S., & Sriboonchitta, S. (2018). Thailand in the era of digital economy: How does digital technology promote economic growth? Predictive Econometrics and Big Data TES2018, 350–362. https://doi.org/10.1007/978-3-319-70942-0_25

Chuttur, M. (2009). Overview of the Technology Acceptance Model: Origins, Developments and Future Directions. Sprouts: Working Papers on Information Systems, 9(37), Article 37.

Davis, F. D. (1989). Technology acceptance model. TAM [Working Paper 529].

Gaur, S., & Tiwari, S. P. (2006). Consumers effortful decision making and self-regulatory orientation. Indian Institute of Technology, 3598–3604. https://doi.org/10.1007/978-3-030-67238-6_5

Gunaratne, H., & Pappel, I. (2020). Enhancement of the e-invoicing systems by increasing the efficiency of workflows via disruptive technologies. International Conference on Electronic Governance and Open Society: Challenges in Eurasia, 60–74.

Hair, J. F., Babin, B. J., Anderson, R. E., & Black, W. C. (2019). Multivariate data analysis (8th ed.). Pearson.

Jantavongso, S., Nuansomsri, C., Kasemsawasdi, S., Anekritmongkol, S., & Sitthikraiwong, S. (2016). eBusiness adoption studies in Thailand. In Knowledge Management International Conference (KMICe) 2016, Chiang Mai, Thailand.

Jongwanich, J. (2022). The economic consequences of globalization on Thailand. Routledge. https://doi.org/10.4324/9781003144076

Khamta, M., & Wattanakulchai, M. (2018). Knowledge and understanding in e-taxation of accounting students in digital 4.0 era. http://dspace.rmutk.ac.th/handle/123456789/2538

Koch, B. (2017). Business case e-invoicing/e-billing. Billentis, 2017, 1–27.

Koch, B. (2019). The e-invoicing journey 2019-2025. Preuzeto, 25, 2021.

Krejcie, R. V., & Morgan, D. W. (1970). Determining sample size for research activities. Educational and Psychological Measurement, 30(3), 607–610. https://doi.org/10.1177/001316447003000308

Lee, M., & Schuele, C. M. (2010). Demographics. Encyclopedia of Research Design, 3, 2–4.

Mamman, M. (2016). Factors Influencing Customer’s Behavioral Intention to Adopt Islamic Banking in Northern Nigeria: A Proposed Framework. IOSR Journal of Economics and Finance (IOSR-JEF), 7(1), Article 1.

Mankhong, G. (2018). A study of components affecting adoption of electronic tax invoice processing and delivery system (e-tax invoice) of entrepreneur In Kamphaeng Phet Province. http://libdoc.dpu.ac.th/thesis/Ganya.Man.pdf

Matsson, E., Dahllöf, G., & Nilsson, J. (2015). Business to business-electronic invoice processing: A report on the challenges, solutions and outcomes for companies switching from manual to electronic invoice handling. Jönköping University.

McCombes, S. (2019). Sampling methods | types, techniques & examples. Scribbr. https://www.scribbr.com/methodology/sampling-methods/

Morshed, A., Ramadan, A., Maali, B., Khrais, L., & Baker, A. (2024). Transforming accounting practices: The impact and challenges of business intelligence integration in invoice processing. Journal of Infrastructure, Policy and Development, 8(6), 4241. https://doi.org/10.24294/jipd.v8i6.4241

Nunnally, J. C. (1978). An overview of psychological measurement. Clinical Diagnosis of Mental Disorders: A Handbook, 97–146. https://doi.org/10.1007/978-1-4684-2490-4_4

Panithanrakchai, W., & Penwutikul, P. (2020). Itthiphon khong thaksa dan phasi akon thi songphon to prasitthiphap kanpatibat ngan nai rabop bai kamkab phasi elektronik thang imeo khong phu tham banchee nai khet Krung Thep Maha Nakhon lae parimonthon [The influence of tax skills on work efficiency in the electronic tax invoice via email system of accountants in Bangkok and metropolitan areas]. Mahachula Academic Journal, 7(2), Article 2.

Pantucha, N. (2020). Effects of tax system and e-documents success on accounting operational efficiency of electronic tax registrants. http://202.28.34.124/dspace/handle123456789/1190

Phonthanukitithaworn, C., Sellitto, C., & Fong, M. W. (2016). An investigation of mobile payment (m-payment) services in Thailand. Asia-Pacific Journal of Business Administration, 8(1), 37–54. https://doi.org/10.1108/APJBA-10-2014-0119

Salkind, N. J., & Frey, B. B. (2021). Statistics for people who (think they) hate statistics: Using Microsoft Excel. Sage publications.

Sawyer, S. F. (2009). Analysis of variance: The fundamental concepts. Journal of Manual & Manipulative Therapy, 17(2), 27E-38E. https://doi.org/10.1179/jmt.2009.17.2.27E

Sharma, L. R. (2023). Choosing appropriate probability sampling designs in research. Health, 2, 4–21.

Singh, A. S., & Masuku, M. B. (2014). Sampling techniques & determination of sample size in applied statistics research: An overview. International Journal of Economics, Commerce and Management, 2(11), 1–22.

Smith, A. (2024). 1776 An Inquiry into the Nature and Causes of the Wealth of Nations. In Foundations of Monetary Economics, Vol. 1 (pp. 223–295). Routledge. https://doi.org/10.4324/9781003552246-6

Sondakh, J. (2017). Behavioral intention to use e-tax service system: An application of technology acceptance model. European Research Studies Journal, 20(2A), Article 2A.

Stolzenberg, R. M. (2004). Multiple regression analysis. Handbook of data analysis, 165–207. https://doi.org/10.4135/9781848608184.n8

Suki, N., & Ramayah, T. (2010). User Acceptance of the e-government services in Malaysia: Structural equation modelling approach. Interdisciplinary Journal of Information, 5, 395–413. https://doi.org/10.28945/1308

Sukkomol, S. (2019). Factor Affecting Acceptance of Technology and Decision to Use e-Tax Invoice & e-Receipt [Unpublished master' s thematic paper]. College of Innovative Business and Accountancy, Dhurakij Pundit University.

Susanto, T. D., Diani, M. M., & Hafidz, I. (2017). User acceptance of e-government citizen report system (a case study of city113 app). Procedia Computer Science, 124, 560–568. https://doi.org/10.1016/j.procs.2017.12.190

Tan, M., & Teo, T. S. (2000). Factors influencing the adoption of Internet banking. Journal of the Association for Information Systems, 1(1), 5. https://doi.org/10.17705/1jais.00005

Teerapunyachai, B., & Bawornkitchaikul, Y. (2024). Innovations and resilience in Thailand’s payment ecosystem: A comprehensive analysis—Connectivity initiatives, challenges and solutions. Journal of Digital Banking, 9(1), 67–85. https://doi.org/10.69554/ASFL8618

Venkatesh, V., & Bala, H. (2008). Technology acceptance model 3 and a research agenda on interventions. Decision Sciences, 39(2), 273–315. https://doi.org/10.1111/j.1540-5915.2008.00192.x

Venkatesh, V., & Davis, F. D. (2000). A theoretical extension of the technology acceptance model: Four longitudinal field studies. Management Science, 46(2), 186–204. https://doi.org/10.1287/mnsc.46.2.186.11926

Vu, K., & Nguyen, T. (2024). Exploring the contributors to the digital economy: Insights from Vietnam with comparisons to Thailand. Telecommunications Policy, 48(1), 102664. https://doi.org/10.1016/j.telpol.2023.102664

Wailerdsak, N. (2023). Business groups and the Thailand economy: Escaping the middle-income trap. Routledge. https://doi.org/10.4324/9781003370536

Yutthana, S. (2021). Tax digitization in Thailand: The new change of e-tax invoice from ‘Analog’ to “Digital.” https://www.itax.in.th/media/tax-digitization-in-thailand-the-new-change-of-e-tax-invoice-from-analog-to-digital/

ดาวน์โหลด

เผยแพร่แล้ว

รูปแบบการอ้างอิง

ฉบับ

ประเภทบทความ

สัญญาอนุญาต

ลิขสิทธิ์ (c) 2025 คณะบริหารธุรกิจ สถาบันบัณฑิตพัฒนบริหารศาสตร์

อนุญาตภายใต้เงื่อนไข Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.