ผลกระทบของการรับรู้รายได้โดยการใช้มาตรฐานการรายงานทางการเงินไทยฉบับที่ 15 (TFRS 15) ที่มีต่อคุณภาพกำไรของบริษัทจดทะเบียนในตลาดหลักทรัพย์แห่งประเทศไทย

คำสำคัญ:

มาตรฐานการรายงานทางการเงิน ฉบับที่ 15, การเปลี่ยนแปลงของรายได้, คุณภาพกำไร, รายการคงค้างบทคัดย่อ

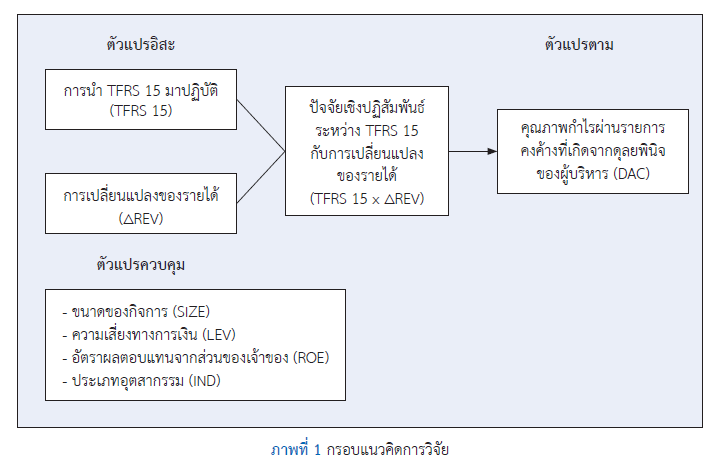

บทความนี้มีวัตถุประสงค์เพื่อ 1. ศึกษาผลกระทบการเปลี่ยนแปลงของรายได้ที่มีต่อคุณภาพกำไร โดยพิจารณาจากปัจจัยเชิงปฏิสัมพันธ์ระหว่างการนำมาตรฐานการรายงานทางการเงินไทยฉบับที่ 15 มาปฏิบัติ (TFRS 15) กับการเปลี่ยนแปลงของรายได้ผ่านรายการคงค้างที่เกิดจากดุลยพินิจของผู้บริหารและ 2. เพื่อศึกษาความแตกต่างของคุณภาพกำไรผ่านรายการคงค้างที่เกิดจากดุลยพินิจของผู้บริหารจากผลกระทบการเปลี่ยนแปลงของรายได้ก่อนและหลังการนำ TFRS 15 มาปฏิบัติ ของบริษัทจดทะเบียนในตลาดหลักทรัพย์แห่งประเทศไทย ตามแบบจำลอง เดอะ มอดิฟายด์ โจนส์ และ แบบจำลอง ยุน มิลเลอร์ และจิราภรณ์ โดยเก็บข้อมูลได้ทั้งสิ้น 319 บริษัท เป็นระยะเวลา 5 ปี ถือเป็นกลุ่มตัวอย่าง 1,595 บริษัท และการวิเคราะห์ข้อมูลงบการเงินของบริษัทจะเป็นปี พ.ศ. 2561 ถึง ปี พ.ศ. 2564 โดยปี พ.ศ. 2561 เป็นปีก่อนการบังคับใช้ ปี พ.ศ. 2562 เป็นปีที่มีผลบังคับใช้ และ ปี พ.ศ. 2563 ถึง ปี พ.ศ. 2564 เป็นปีหลังการบังคับใช้ เพื่อนำมาวิเคราะห์สถิติเชิงพรรณนาและสถิติเชิงอนุมาน โดยใช้เทคนิควิเคราะห์การถดถอยเชิงพหุคุณและการวิเคราะห์กลุ่มตัวอย่าง 2 กลุ่มที่สัมพันธ์กัน

ผลการวิจัยพบว่า 1) ตามแบบจำลอง เดอะ มอดิฟายด์ โจนส์ การนำ TFRS 15 มาปฏิบัติ ปัจจัยเชิงปฏิสัมพันธ์ระหว่าง TFRS 15 กับการเปลี่ยนแปลงของรายได้ ทำให้คุณภาพกำไรผ่านรายการคงค้างที่เกิดจากดุลยพินิจของผู้บริหารมีระดับสูงขึ้นอย่างมีนัยสำคัญทางสถิติ แต่อย่างไรก็ตาม 2) หากวิเคราะห์ตามแบบจำลอง ยุน, มิลเลอร์, และจิราภรณ์ พบว่า การนำ TFRS 15 มาปฏิบัติ ปัจจัยเชิงปฏิสัมพันธ์ระหว่างตัวแปรทั้งสองข้างต้น ทำให้คุณภาพกำไรผ่านรายการคงค้างที่เกิดจากดุลยพินิจของผู้บริหารมีระดับสูงขึ้น แต่ไม่มีนัยสำคัญทางสถิติ และ 3) ปีก่อน (พ.ศ. 2561) และปีหลัง (พ.ศ. 2562) ของการนำ TFRS 15 มาปฏิบัติมีความแตกต่างกันของค่าเฉลี่ยคุณภาพกำไรผ่านรายการคงค้างที่เกิดจากดุลยพินิจของผู้บริหารจากผลกระทบการเปลี่ยนแปลงของรายได้ ตามแบบจำลอง เดอะ มอดิฟายด์ โจนส์ และ แบบจำลอง ยุน, มิลเลอร์, และจิราภรณ์ ซึ่งนักลงทุนและผู้มีส่วนได้เสียสามารถทราบถึงข้อมูล วิธีการ และผลลัพธ์ของคุณภาพกำไร พร้อมทั้งสามารถเปรียบเทียบผลกระทบของคุณภาพกำไรก่อนและหลังการนำมาตรฐานการรายงานทางการเงิน ฉบับที่ 15 มาปฏิบัติ

เอกสารอ้างอิง

Alareeni, B., & Aljuaidi, O. (2014). The modified Jones and Yoon models in detecting earnings management in Palestine exchange (PEX). International Journal of Innovation and Applied Studies, 9(4), 1472-1484.

Aziz, N., & Acma, N. M. (2018). The contemporary issues on new revenue recognition standard. AIUB International Conference on Business and Management. Dhaka, Bangladesh.

Bartov, E., Gul, F. A., & Tsui, J. S. L. (2000). Discretionary-accruals models and audit qualifications. Journal of Accounting and Economics, 30(3), 421-452. https://doi.org/10.2139/ssrn.214996

Becker, C. L., DeFond, M. L., Jiambalvo, J., & Subramanyam, K. R. (1998). The effect of audit quality on earnings management. Contemporary Accounting Research, 15(1), 1-24. https://doi.org/10.1111/j.1911-3846.1998.tb00547.x

Chavanwan, W., & Srijunpetch, S. (2020). The effect of applying TFRS 15 revenue from contracts with customers on earning quality. Journal of Accounting Professions. 16(51), 5-22.

DeChow, P. M., Sloan, R. G., & Sweeney, A. P. (1995). Detecting earnings management.The Accounting Review, 70(2), 193-225.

Gujarati, D. N., & Porter, D. C. (2009). Basic econometrics (5th ed.). McGraw-Hill.

Habib, A., & Azim, I. (2008). Corporate governance and the value-relevance of accounting information: evidence from Australia. Accounting Research Journal, 21(2), 167-194. https://doi.org/10.1108/10309610810905944

Hameed, A. M. (2019). The impact of IFRS 15 on earnings quality in businesses such as hotels: Critical evidence from the Iraqi environment. African Journal of Hospitality, Tourism and Leisure, 8(4), 1-11.

Jantadej, K. (2014). Revenue from contracts with customers: New model of revenue recognition. Journal of Accounting Profession, 10(27), 45-63.

Kaewkerd, S. (2014). Analysis of earnings quality and efficiency in the operations of listed companies in the stock exchange of Thailand, food industry [Unpublished doctoral dissertation]. North Bangkok University.

Kasznik, R. (1999). On the association between voluntary disclosure and earnings management. Journal of Accounting Research, 37(1), 57-81. https://doi.org/10.2307/2491396

Kim, Y., Liu, C., & Rhee, S. G. (2003). The effect of firm size on earnings management. University of Hawaii.

Klein, A. (2002). Audit committee, board of director characteristics, and earnings management. Journal of Accounting and Economics, 33(3), 375-400. https://doi.org/10.1016/S0165-4101(02)00059-9

Krassanairawiwong, K. (2019). TFRS 15 adoption on earnings quality in the sectors of Thailand property and construction [Unpublished independent study]. Thammasat University.

Krassanairawiwong, K., & Srijunpetch, S. (2020). The effect of adoption Thai financial reporting standard 15 revenue from contract with customers on earnings quality of companies in the property and construction sectors in stock exchange of Thailand. Journal of Business Administration The Association of Private Higher Education Institutions of Thailand, 9(2), 117-128.

Kothari, S. P., Leone, A. J., & Wasley, C. E. (2005). Performance matched discretionary accrual measures. Journal of Accounting and Economics, 39(1), 163-197.https://doi.org/10.1016/j.jacceco.2004.11.002

Liu, Z-J., & Wang, Y-S. (2017). Effect of earnings management on economic value added: G20 and African countries study. South African Journal of Economic and Management Sciences, 20(1), 1-9. https://doi.org/10.4102/sajems.v20i1.1247

Neerapattanakun, D. (2023). How does the implementation of TFRS 15 revenue from contracts with customers affect the change from the application? Journal of Humanities and Social Sciences Nakhon Phanom University, 13(2), 96-113.

Prom-In, D., & Dampitakse, K. (2018). Relationship among performance and earnings quality on market stock price of listed companies in the stock exchange of Thailand in the technology industry group. MBA-KKU Journal, 11(2), 37-59.

Roonghuaphai, R., & Dampitakse, K. (2019). Analysis of earnings quality and security returns of listed companies in the stock exchange of Thailand. Santapol College Academic Journal, 5(2), 213-225.

Srijunpetch, S., & Phakdee, A. (2019). Revenue from contracts with customers: Revenue recognition principles. Journal of Federation of Accounting Professions, 1(1), 4-20.

Srijunpetch, S., & Phakdee, A. (2020). How did the first year of TFRS 15 implementation have an impact on the financial statements?. Journal of Accounting Professions, 16(50), 23-42.

Stevens, J. (1992). Applied multivariate statistics for the social sciences (2nd ed.). Harper and Row.

The Stock Exchange of Thailand. (2022). Company information listed on the Stock Exchange of Thailand. https://www.set.or.th/th/market/information/securities-list/main

Yishu, W., Xue, J., ZhenJia, L., & Weixing, W. (2015). Effect of earnings management on economic value added: A China study. Accounting and Finance Research, 4(3), 9-19. https://doi.org/10.5430/afr.v4n3p9

Yoon, S. S., Miller, G., & Jiraporn, P. (2006). Earnings management vehicles for Korean firms. Journal of International Financial Management and Accounting, 17(2), 85-109. https://doi.org/10.1111/j.1467-646X.2006.00122.x

ดาวน์โหลด

เผยแพร่แล้ว

รูปแบบการอ้างอิง

ฉบับ

ประเภทบทความ

สัญญาอนุญาต

ลิขสิทธิ์ (c) 2025 คณะบริหารธุรกิจ สถาบันบัณฑิตพัฒนบริหารศาสตร์

อนุญาตภายใต้เงื่อนไข Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.