การประยุกต์ใช้เทคนิคการวิเคราะห์องค์ประกอบหลักเพื่อการจัดกลุ่มหลักทรัพย์ลงทุน ด้วย Global ETF

คำสำคัญ:

การเลือกพอร์ตการลงทุน, การกระจายกลุ่มธุรกิจ, การกระจายพอร์ตการลงทุน, ทฤษฎีพอร์ตโฟลิโอสมัยใหม่, การวิเคราะห์องค์ประกอบหลักบทคัดย่อ

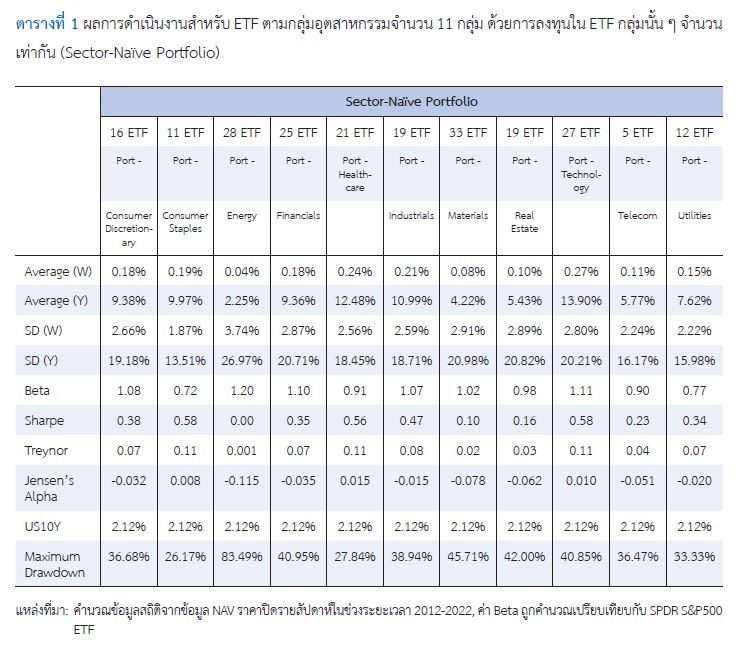

การศึกษานี้มีวัตถุประสงค์เพื่อศึกษาแนวทางการประยุกต์ใช้เทคนิคการวิเคราะห์องค์ประกอบหลัก หรือ Principal Component Analysis (PCA) ในการเลือกพอร์ตการลงทุนในแต่ละกลุ่มธุรกิจด้วย Global ETF เมื่อศึกษาข้อมูลราคาหลักทรัพย์รายสัปดาห์สำหรับ Global ETF ทั้งหมดจำนวน 216 กองทุน ในระหว่างปี ค.ศ. 2012 – 2022 พบว่า กลุ่มธุรกิจที่ให้ผลตอบแทนสูงสุดคือ กลุ่ม Technology และผลตอบแทนต่ำที่สุดคือ Energy ในด้านความเสี่ยงสูงที่สุดคือ Energy และความเสี่ยงต่ำที่สุดคือ Consumer Staples หลังจากใช้การทดลองคัดแยกองค์ประกอบหลักด้วยเทคนิค PCA พบว่า เทคนิค PCA สามารถคัดเลือกตัวแทนจากกลุ่มธุรกิจมาจัดเป็นพอร์ตการลงทุนโดยมีค่าสหสัมพันธ์ (Correlation) ระหว่าง ETF แต่ละตัวที่มาสร้างพอร์ตการลงทุนโดยมีค่าเฉลี่ยรวมอยู่ที่ 0.45 เท่านั้น หลังจากใช้เทคนิค PCA ผสมผสานกับ MPT ภายใต้วัตถุประสงค์ที่ทำให้ค่า Sharpe Ratio ของพอร์ตสูงสุด และมีข้อจำกัดในการห้ามทำการขายชอร์ต (Short Sell) โดยกำหนดรูปแบบน้ำหนักการลงทุนแบบเพิ่มเพดานน้ำหนักการ ลงทุน พบว่า การเพิ่มน้ำหนักการลงทุน ETF ตามหมวดธุรกิจ 2 หมวดคือ Consumer Staples Equities โดยเพิ่มน้ำหนักการลงทุนตั้งแต่ 10%-50% และหมวด Technology Equities ในกลุ่มธุรกิจ Semiconductor โดยเพิ่มน้ำหนัก การลงทุนตั้งแต่ 3%-17% สามารถสร้างผลตอบแทนที่ดีขึ้น

เอกสารอ้างอิง

Canak, B., & Yilmaz, M. (2020). Principal Component Analysis (PCA) and its applications in stock portfolio selection and optimization. Journal of Financial Research, 33(1), 112-130.

Chen, H. (2014). Portfolio construction using Principal Component Analysis (Master’s project) Worcester Polytechnic Institute, United States.

Chicheportiche, R., & Bouchaud, J.-P. (2020). Nonlinear dynamics and criticality in financial markets. Journal of Statistical Mechanics: Theory and Experiment, 2020(8), 083403.

Gupta, R., & Basu, P. K. (2009). Sector analysis and portfolio optimization: The Indian experience. International Journal of Economics and Business Research, 8(1), 19-130. https://doi.org/10.19030/iber.v8i1.3096

Kaiser, H. F. (1960). The application of electronic computers to factor analysis. Educational and Psychological Measurement, 20, 141-151. https://doi.org/10.1177/001316446002000116

Kapoor, A. (2012). Diversification benefits of sector investments in Indian capital market. International Journal of Business and Management Cases, 1(2). https://doi.org/10.2139/ssrn.2067934

Komain Jiranyakul. (2002). Kānbō̜rihānkhwāmsīangnaiphō̜takānlongthun [Portfolio management strategy]. Thai Journal of Development Administration, 42 (Special Issue NIDA 36th Anniversary), 131-168. (in Thai)

Markowitz, H. (1952). Portfolio selection. The Journal of Finance, 7(1), 77-91. https://doi.org/10.2307/2975974

Meric, I., Dunne, K., McCall, C. W., & Meric, G. (2010). Performance of exchange-traded sector index funds in the October 9, 2007–March 9, 2009 bear market. Journal of Finance and Accountancy, 3, 1-10.

Meric, I. [Ilhan], Ding, J., & Meric, G. [Gulser]. (2016). Global portfolio diversification with emerging stock markets. Emerging Markets Journal, 6(1). https://doi.org/10.5195/emaj.2016.88

Meric, I., Dunne, K., McCall, C. W., & Meric, G. (2023). Hierarchical PCA and applications to portfolio management. Journal of Financial Data Science, 11(4), 240-257.

Piedboeuf, C. (2023). Portfolio Selection via Principal Component Analysis. Louvain School of Management, Université catholique de Louvain. Retrieved from Louvain Repository.

Roncalli, T. (2010). Understanding the impact of weights constraints in portfolio theory (Research & development). Evry University, Paris. https://doi.org/10.2139/ssrn.1761625

Sharma, R. (2023). Sectoral portfolio optimization by judicious selection of financial ratios via PCA. Journal of Financial Analysis, 48(2), 85-102.

Tan, J. (2012). Principal component analysis and portfolio optimization (Applied finance project). University of California, Berkeley. https://doi.org/10.2139/ssrn.2213687

Terada Pinyo. (2018). Theknik kān plǣ phon kān wikhro̜ ʻongprakō̜p samrap ngānwičhai [Techniques for interpreting factor analysis results for research]. Panyapiwat Journal, 10(Special Issue), 292-304. (in Thai)

ดาวน์โหลด

เผยแพร่แล้ว

รูปแบบการอ้างอิง

ฉบับ

ประเภทบทความ

สัญญาอนุญาต

ลิขสิทธิ์ (c) 2024 คณะบริหารธุรกิจ สถาบันบัณฑิตพัฒนบริหารศาสตร์

อนุญาตภายใต้เงื่อนไข Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.