ESG Performance and Analyst Forecast Accuracy: Evidence from SET100 Index

Keywords:

ESG, Analyst Forecast Accuracy, Financial Analysts, SET100Abstract

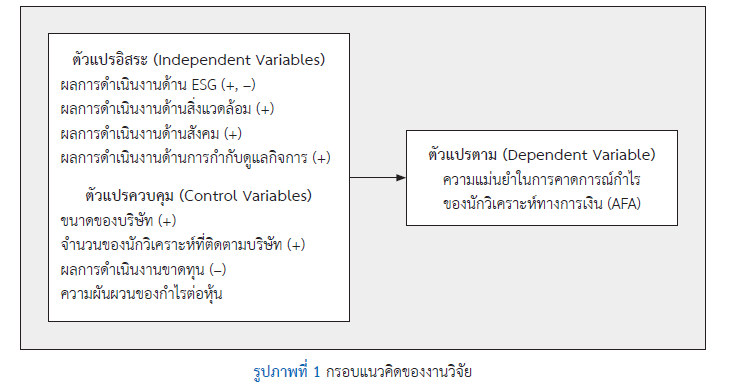

This study aimed to examine the relationship between overall Environmental, Social, and Governance (ESG) performance, as well as its individual dimensions, and analysts’ earnings forecast accuracy of firms listed on the Stock Exchange of Thailand (SET) in the SET100 Index. The sample consisted of 342 firm-year observations covering the period 2020–2024. The analysis employed a multiple regression model under a Fixed Effects framework with firm-clustered robust standard errors to control for unobserved firm-specific characteristics and autocorrelation.

The results indicated that overall ESG performance was positively associated with analysts’ earnings forecast accuracy at the 5% significance level. This finding suggested that improvements in ESG performance enhanced the information environment, enabling financial analysts to produce more accurate earnings forecasts. The evidence supported Signaling Theory and Information Asymmetry Theory, implying that high-quality ESG disclosure reduced information gaps and strengthened the overall information environment in the Thai capital market.

In sum the findings suggested that the overall development of transparent, consistent, and high-quality ESG disclosure standards could improve the efficiency of financial analysis and firm valuation in the long run. However, when ESG was examined by dimension, social had the strongest effect on forecast accuracy, followed by environmental, while governance was not significant, suggesting that stakeholder-related social information most effectively reduces information asymmetry.

References

Akerlof, G. A. (1970). The market for “lemons”: Quality uncertainty and the market mechanism. The Quarterly Journal of Economics, 84(3), 488-500. https://doi.org/10.2307/1879431

Ayem, S., Kusuma, H., & Arifin, J. (2024). Integrated reporting, ESG disclosure, forecast accuracy, and firm value: Profitability as moderating variable. Journal of Lifestyle and SDGs Review, 5(2). https://doi.org/10.47172/2965-730X.SDGsReview.v5.n02.pe02608

Bhat, G., Hope, O.-K., & Kang, T. (2006). Does corporate governance transparency affect the accuracy of analyst forecasts? Accounting & Finance, 46(5), 715-732. https://doi.org/10.1111/j.1467-629X.2006.00191.x

Bradshaw, M. T. (2011). Analysts’ forecasts: What do we know after decades of work? SSRN Electronic Journal. https://doi.org/10.2139/ssrn.1880339

Byard, D., Li, Y., & Weintrop, J. (2006). Corporate governance and the quality of financial analysts’ information. Journal of Accounting and Public Policy, 25(5), 609-625. https://doi.org/10.1016/j.jaccpubpol.2006.07.003

Clarkson, P. M., Li, Y., Richardson, G. D., & Vasvari, F. P. (2013). The relevance of environmental disclosures for investors and other stakeholder groups: Are such disclosures incrementally informative? Journal of Accounting and Public Policy, 32(5), 410-431. https://doi.org/10.1016/j.jaccpubpol.2013.06.008

Cohen, J. (1988). Statistical power analysis for the behavioral sciences (2nd ed.). Lawrence Erlbaum Associates.

Connelly, B. L., Certo, S. T., Ireland, R. D., & Reutzel, C. R. (2011). Signaling theory: A review and assessment. Journal of Management, 37(1), 39-67. https://doi.org/10.1177/

Dhaliwal, D. S., Radhakrishnan, S., Tsang, A., & Yang, Y. G. (2012). Nonfinancial disclosure and analyst forecast accuracy: International evidence on corporate social responsibility disclosure. The Accounting Review, 87(3), 723-759. https://doi.org/10.2308/accr-10218

Eccles, R. G., Ioannou, I., & Serafeim, G. (2014). The impact of corporate sustainability on organizational processes and performance. Management Science, 60(11), 2835-2857. https://doi.org/10.1287/mnsc.2014.1984

Ernstberger, J., & Grüning, M. (2013). How do firm- and country-level governance mechanisms affect firms' disclosure? Journal of Accounting and Public Policy, 32(3), 50-67. https://doi.org/10.1016/j.jaccpubpol.2013.02.003

Freeman, R. E. (1984). Strategic management: A stakeholder approach. Pitman.

Givoly, D., & Lakonishok, J. (1984). The quality of analysts’ forecasts of earnings. Financial Analysts Journal, 40(5), 40-47.

Gujarati, D. N., & Porter, D. C. (2009). Basic econometrics (5th ed.). McGraw-Hill Education.

Healy, P. M., & Palepu, K. G. (2001). Information asymmetry, corporate disclosure, and the capital markets: A review of the empirical disclosure literature. Journal of Accounting and Economics, 31(1–3), 405-440. https://doi.org/10.1016/S0165-4101(01)00018-0

Li, K. (2024). ESG performance and analyst forecast accuracy: A moderating role of economic uncertainty [Master’s thesis, University of Amsterdam]. https://scripties.uba.uva.nl/download?fid=c11220320

Liu, S. (2016). Ownership structure and analysts’ forecast properties: A study of Chinese listed firms. Corporate Governance, 16(1), 54-78. https://doi.org/10.1108/CG-02-2015-0018

Lozano, R. (2008). Envisioning sustainability three-dimensionally. Journal of Cleaner Production, 16(17), 1838-1846. https://doi.org/10.1016/j.jclepro.2008.02.008

Luo, L., & Wu, H. (2022). Corporate sustainability and analysts' earnings forecast accuracy: Evidence from environmental, social and governance ratings. Corporate Social Responsibility and Environmental Management, 29(5), 1465-1481. https://doi.org/10.1002/csr.2284

Michelon, G., Pilonato, S., & Ricceri, F. (2015). CSR reporting practices and the quality of disclosure: An empirical analysis. Critical Perspectives on Accounting, 33, 59-78. https://doi.org/10.1016/j.cpa.2014.10.003

Spence, M. (1973). Job market signaling. The Quarterly Journal of Economics, 87(3), 355–374.

Thai, H. M., Thu, T. H. T., Ngoc, S. P., & Thi, A. M. (2023). Corporate governance and the accuracy of analysts' earnings forecast in Vietnam. In Proceedings of the International Conference on Emerging Challenges: Strategic Adaptation in the World of Uncertainties (ICECH 2022) (pp. 442–466). Atlantis Press. https://doi.org/10.2991/978-94-6463-150-0_29

Thai Institute of Directors. (2024). Corporate governance report of Thai listed companies 2024. Thai Institute of Directors.

The Securities and Exchange Commission of Thailand. (2021). Guideline for preparing the annual registration statement/annual report. The Securities and Exchange Commission of Thailand.

The Stock Exchange of Thailand. (2025a). Sustainable capital market development. The Stock Exchange of Thailand.

The Stock Exchange of Thailand. (2025b). Sustainable investment. The Stock Exchange of Thailand.

Wooldridge, J. M. (2016). Introductory econometrics: A modern approach (6th ed.). Cengage Learning.

Zhang, J. (2024). Greenwashing and analyst forecast accuracy: Evidence from China’s listed firms [Master’s thesis, Macquarie University]. https://doi.org/10.25949/

Downloads

Published

How to Cite

Issue

Section

License

Copyright (c) 2026 NIDA Business School, National Institute of Development Administration

This work is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.