The Impact of Board Interlocking on the Market Value Added of Listed Companies on the Stock Exchange of Thailand: The Moderating Effect of Managerial Ownership

Keywords:

Board Interlocking, Market value added, Managerial Ownership, The Stock Exchange of ThailandAbstract

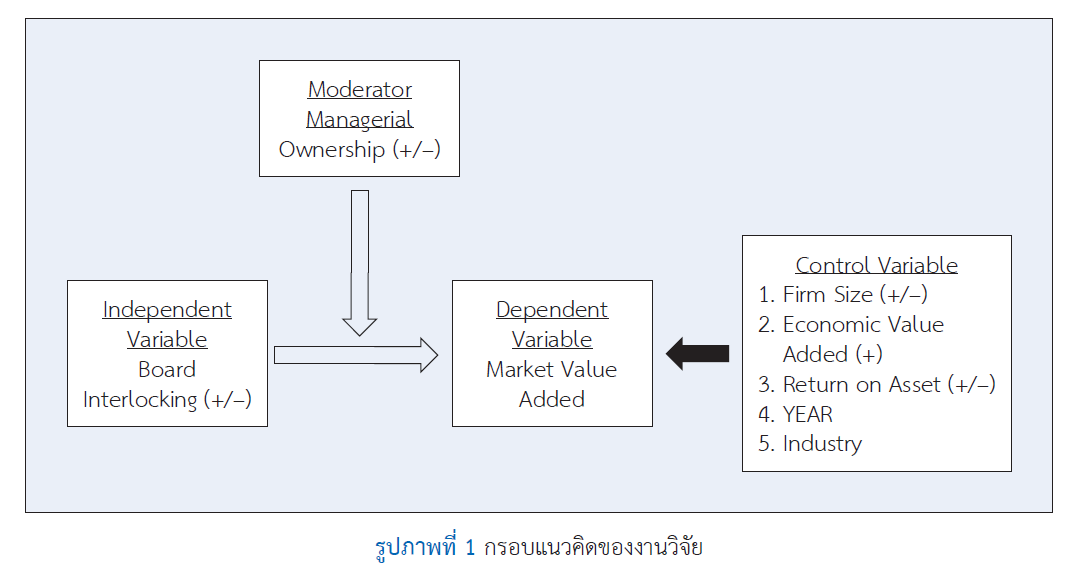

This study aims to examine the impact of board interlocking on market value added (MVA), with managerial ownership serving as a moderating variable. The sample consists of 1,350 firm-year observations from 450 listed companies on the Stock Exchange of Thailand from 2021 to 2023. Both descriptive and inferential statistics were used for data analysis. This study utilized a multiple regression model based on the Pooled Ordinary Least Squares (Pooled OLS) method.

The findings reveal that board interlocking is positively associated with market value added at the 5% significance level. This suggests that directors holding positions across multiple firms can significantly enhance firms’ market value added, in line with the Resource Dependence Theory. Furthermore, the results indicate that managerial ownership negatively moderates the relationship between board interlocking and market value added, at the 5% significance level. In other words, as the proportion of managerial ownership increases, the value enhancing effect of board interlocking diminishes. This finding aligns with Agency Theory, which highlights the potential risk of managerial behavior that may diverge from shareholder interests. In addition, the study finds that firm size is negatively associated with market value added, whereas return on assets exhibits a positive relationship with market value added.

References

Adsakul, N. (2015). Performance measures affecting economic value added and market value added of company in services industry group in the Stock Exchange of Thailand [Master’s thesis, Sripatum University].

Biswas, S., Sarkar, J., & Selarka, E. (2023). Women director interlocks and firm performance: Evidence from India (Working Paper No. WP-2023-016). Indira Gandhi Institute of Development Research. https://doi.org/10.2139/ssrn.4653412

Dal Vesco, D. G., & Beuren, I. M. (2016). Do the board of directors composition and the board interlocking influence on performance? BAR-Brazilian Administration Review, 13(2) Article 1, e160007. http://dx.doi.org/10.1590/1807-7692bar2016160007

Dawson, J. F. (2013). Moderation in management Research: What, why, when, and how. Journal of Business and Psychology, 29(1), 1-19. https://doi.org/10.1007/s10869-013-9308-7

Dee-Arsa, P., & Sittipatna, P. (2024). The relevance of economic value added and financial performance measures on the market value added of companies in the sustainable stock price movement index group list in the Stock Exchange of Thailand. Western University Research Journal of Humanities and Social Science, 10(1), 113-126.

Drucker, P. (1993). Post-capitalist society. Butterworth-Heinemann.

Edacherian, S., Richter, A., Karna, A., & Gopalakrishnan, B. (2023). Connecting the right knots: The impact of board committee interlocks on the performance of Indian firms. Corporate Governance an International Review, 32(1), 135-155. https://doi.org/10.1111/corg.12523

Farwis, M., & Nazar, M. C. A. (2019). Interlocking directorate and firm performance of listed companies in Sri Lanka. Asian Journal of Research in Banking and Finance, 9(3), 1-15. https://doi.org/10.5958/2249-7323.2019.00003.8

Gujarati, D. N., & Porter, D. C. (2009). Basic econometrics (5th ed.). McGraw-Hill Education.

Hamdan, A. (2018). Board interlocking and firm performance: The role of foreign ownership in Saudi Arabia. International Journal of Managerial Finance, 14(3), 266-281. https://doi.org/10.1108/IJMF-09-2017-0192

Haunschild, P., & Beckman, C. (1998). When do interlocks matter? Alternate sources of information and interlock influence. Administrative Science Quarterly, 43(4), 815-845. https://doi.org/10.2307/2393617

Ifada, L. M., Fuad, K., & Kartikasari, L. (2021). Managerial ownership and firm value: The role of corporate social responsibility. Jurnal Akuntansi dan Auditing Indonesia, 25(2), 162-171. https://doi.org/10.20885/jaai.vol25.iss2.art6

Jensen, M. C., & Meckling, W. H. (1976). Theory of the firm: Managerial behavior, agency costs and ownership structure. Journal of Financial Economics, 3(4), 305-360. https://doi.org/10.1016/0304-405X(76)90026-X

Jetiya, A., Kawewong, N., & Diskulnetivitya, P. (2022). Impact of economic value added and financial ratios towards market value added of listed companies in SET100 Index. Journal of Administrative and Management Innovation, 10(1), 24-33.

Morck, R., Shleifer, A., & Vishny, R. W. (1988). Management ownership and market valuation: An empirical analysis. Journal of Financial Economics, 20, 293-315. https://doi.org/10.1016/0304-405X(88)90048-7

Park, J. H. (2025). The impact of interlocking directorates on firm value: Empirical evidence from KOSDAQ companies in Korea. Global Business & Finance Review, 30(1), 100-115. https://doi.org/10.17549/gbfr.2025.30.1.100

Peng, M. W., Mutlu, C. C., Sauerwald, S., Au, K. Y., & Wang, D. Y. L. (2015). Board interlocks and corporate performance among firms listed abroad. Journal of Management History, 21(2), 257-282. https://doi.org/10.1108/JMH-08-2014-0132

Pfeffer, J., & Salancik, G. R. (1978). The external control of organizations: A resource dependence approach. Harper and Row Publishers.

Sany, C., Novica, C., & Valentina, C. (2024). Do board multiple directorships and ESG score drive firm value? Study of non-financial companies in Thailand. Jurnal Akuntansi dan Keuangan, 26(1), 67–76. https://doi.org/10.9744/jak.26.1.67-76

Srivardhana, T. (2010). The effects of board interlocking networks: A case study of listed companies in the Stock Exchange of Thailand [Master’s thesis, National Institute of Development Administration].

Stewart, G. B. (1991). The quest for value. Harper Business.

Sukeecheep, S., Yarram, S. R., & Al Farooque, O. (2013, March 20–23). Earnings management and board characteristics in Thai listed companies. The 2013 IBEA International Conference on Business, Economics, and Accounting, Bangkok, Thailand.

Tan, K. M., Bany-Ariffin, A. N., Kamarudin, F., & Abdul Rahim, N. (2019). Does directors’ experience positively moderate the impact of board busyness on firm efficiency? Evidence from Asia-Pacific. Asia-Pacific Journal of Business Administration, 11(3), 232- 250. https://doi.org/10.1108/APJBA-01-2019-0008

The Stock Exchange of Thailand. (2017). Corporate governance code for listed companies. The Stock Exchange of Thailand.

Ullah, W., Ali, S., & Mehmood, S. (2017). Impact of excess control, ownership structure and corporate governance on firm performance of diversified group firms in Pakistan. Business & Economic Review, 9(2), 49–72. https://doi.org/10.22547/BER/9.2.3

Venkatesh, G., Kshatriya, S., & Bansal, S. (2024). Board busyness and firm performance: An emerging market perspective. Corporate Governance: An International Review, 33(2), 231-245. https://doi.org/10.1111/corg.12600

Young, S. D., & O’Byrne, S. F. (2001). EVA and value based management. McGraw Hill.

Downloads

Published

How to Cite

Issue

Section

License

Copyright (c) 2025 NIDA Business School, National Institute of Development Administration

This work is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.