The Impact of Revenue Recognition by Applying Thai Financial Reporting Standard 15 (TFRS 15) on the Earnings Quality of Listed Companies in the Stock Exchange of Thailand

Keywords:

Thai Financial Report Standard No 15 (TFRS 15), Change in Revenue, Earnings Quality, Discretionary AccrualAbstract

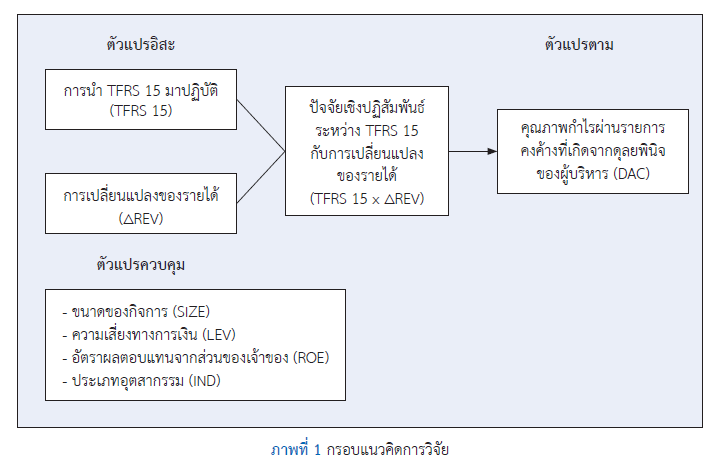

This article aims to study the impact of changes in total revenue on earnings quality by considering the interaction factors between the adoption of Thai Financial Reporting Standards 15 (TFRS 15) and changes in total revenue through discretionary accruals from management's judgment and to study the differences in the earnings quality through discretionary accruals from management’s judgment on the impact of changes in total revenue before and after the adoption of TFRS 15 on the listed companies on the Stock Exchange of Thailand on The Modified Jones model and Yoon, Miller, and Jiraporn model. By collecting data, a total of 319 companies were collected data for a period of 5 years, which is considered as samples of 1,595 companies and analyzed financial statements of companies from 2018 to 2021. 2018 was the year before the enforcement, 2019 was the year that was effective, and 2020 and 2021 were years after the enforcement. To analyze descriptive statistics and inferential statistics, using multiple linear regression analysis and analysis of two related sample groups. Research results are 1) according to the modified Jones model, it was found that by the implementation of TFRS 15, the interaction effect between TFRS 15 and total revenue changes, significantly increased the earnings quality through discretionary accruals from management's judgment, with statistical significance. However, if analyzed 2) according to the Yoon, Miller, and Jiraporn model, it was found that by the implementation of TFRS 15, along with the interaction effect between the previous two variables, increased the earnings quality through discretionary accruals, but without statistical significance. And 3) The year before (2018) and the year after (2019) of the implementation of TFRS 15 have differences on the average quality of the earnings through accruals resulting from management’s judgment according to the impact of income change based on The Modified Jones model and Yoon, Miller, & Jiraporn model. The investors and stakeholders can understand information, methods, and results of profit quality. Besides, it can be used to compare the impact of profit quality before and after the implementation of TFRS 15.

References

Alareeni, B., & Aljuaidi, O. (2014). The modified Jones and Yoon models in detecting earnings management in Palestine exchange (PEX). International Journal of Innovation and Applied Studies, 9(4), 1472-1484.

Aziz, N., & Acma, N. M. (2018). The contemporary issues on new revenue recognition standard. AIUB International Conference on Business and Management. Dhaka, Bangladesh.

Bartov, E., Gul, F. A., & Tsui, J. S. L. (2000). Discretionary-accruals models and audit qualifications. Journal of Accounting and Economics, 30(3), 421-452. https://doi.org/10.2139/ssrn.214996

Becker, C. L., DeFond, M. L., Jiambalvo, J., & Subramanyam, K. R. (1998). The effect of audit quality on earnings management. Contemporary Accounting Research, 15(1), 1-24. https://doi.org/10.1111/j.1911-3846.1998.tb00547.x

Chavanwan, W., & Srijunpetch, S. (2020). The effect of applying TFRS 15 revenue from contracts with customers on earning quality. Journal of Accounting Professions. 16(51), 5-22.

DeChow, P. M., Sloan, R. G., & Sweeney, A. P. (1995). Detecting earnings management.The Accounting Review, 70(2), 193-225.

Gujarati, D. N., & Porter, D. C. (2009). Basic econometrics (5th ed.). McGraw-Hill.

Habib, A., & Azim, I. (2008). Corporate governance and the value-relevance of accounting information: evidence from Australia. Accounting Research Journal, 21(2), 167-194. https://doi.org/10.1108/10309610810905944

Hameed, A. M. (2019). The impact of IFRS 15 on earnings quality in businesses such as hotels: Critical evidence from the Iraqi environment. African Journal of Hospitality, Tourism and Leisure, 8(4), 1-11.

Jantadej, K. (2014). Revenue from contracts with customers: New model of revenue recognition. Journal of Accounting Profession, 10(27), 45-63.

Kaewkerd, S. (2014). Analysis of earnings quality and efficiency in the operations of listed companies in the stock exchange of Thailand, food industry [Unpublished doctoral dissertation]. North Bangkok University.

Kasznik, R. (1999). On the association between voluntary disclosure and earnings management. Journal of Accounting Research, 37(1), 57-81. https://doi.org/10.2307/2491396

Kim, Y., Liu, C., & Rhee, S. G. (2003). The effect of firm size on earnings management. University of Hawaii.

Klein, A. (2002). Audit committee, board of director characteristics, and earnings management. Journal of Accounting and Economics, 33(3), 375-400. https://doi.org/10.1016/S0165-4101(02)00059-9

Krassanairawiwong, K. (2019). TFRS 15 adoption on earnings quality in the sectors of Thailand property and construction [Unpublished independent study]. Thammasat University.

Krassanairawiwong, K., & Srijunpetch, S. (2020). The effect of adoption Thai financial reporting standard 15 revenue from contract with customers on earnings quality of companies in the property and construction sectors in stock exchange of Thailand. Journal of Business Administration The Association of Private Higher Education Institutions of Thailand, 9(2), 117-128.

Kothari, S. P., Leone, A. J., & Wasley, C. E. (2005). Performance matched discretionary accrual measures. Journal of Accounting and Economics, 39(1), 163-197.https://doi.org/10.1016/j.jacceco.2004.11.002

Liu, Z-J., & Wang, Y-S. (2017). Effect of earnings management on economic value added: G20 and African countries study. South African Journal of Economic and Management Sciences, 20(1), 1-9. https://doi.org/10.4102/sajems.v20i1.1247

Neerapattanakun, D. (2023). How does the implementation of TFRS 15 revenue from contracts with customers affect the change from the application? Journal of Humanities and Social Sciences Nakhon Phanom University, 13(2), 96-113.

Prom-In, D., & Dampitakse, K. (2018). Relationship among performance and earnings quality on market stock price of listed companies in the stock exchange of Thailand in the technology industry group. MBA-KKU Journal, 11(2), 37-59.

Roonghuaphai, R., & Dampitakse, K. (2019). Analysis of earnings quality and security returns of listed companies in the stock exchange of Thailand. Santapol College Academic Journal, 5(2), 213-225.

Srijunpetch, S., & Phakdee, A. (2019). Revenue from contracts with customers: Revenue recognition principles. Journal of Federation of Accounting Professions, 1(1), 4-20.

Srijunpetch, S., & Phakdee, A. (2020). How did the first year of TFRS 15 implementation have an impact on the financial statements?. Journal of Accounting Professions, 16(50), 23-42.

Stevens, J. (1992). Applied multivariate statistics for the social sciences (2nd ed.). Harper and Row.

The Stock Exchange of Thailand. (2022). Company information listed on the Stock Exchange of Thailand. https://www.set.or.th/th/market/information/securities-list/main

Yishu, W., Xue, J., ZhenJia, L., & Weixing, W. (2015). Effect of earnings management on economic value added: A China study. Accounting and Finance Research, 4(3), 9-19. https://doi.org/10.5430/afr.v4n3p9

Yoon, S. S., Miller, G., & Jiraporn, P. (2006). Earnings management vehicles for Korean firms. Journal of International Financial Management and Accounting, 17(2), 85-109. https://doi.org/10.1111/j.1467-646X.2006.00122.x

Downloads

Published

How to Cite

Issue

Section

License

Copyright (c) 2025 NIDA Business School, National Institute of Development Administration

This work is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.